In our previous post — Red Sea Crisis 2026: How the Iran War Is Choking Global Trade — we examined how Operation Epic Fury and the resulting dual-chokepoint crisis are strangling global shipping lanes, sending freight rates through the ceiling and disrupting supply chains across every continent. If you haven’t read it yet, it is essential context for everything that follows.

But the disruption does not end at the docks.

While container ships divert around Africa and tankers sit stranded in the Strait of Hormuz, a parallel crisis is unfolding in the world’s financial markets — one that is arguably more structurally dangerous and far less understood. The Iran war has done something extraordinary: it has simultaneously broken down the traditional correlation between stocks, bonds, gold, and the dollar — the foundational logic that underpins how institutions, funds, and individual investors manage risk.

Every experienced trader, CFO, and portfolio manager knows the classic geopolitical crisis playbook: sell equities, buy bonds, buy gold, watch oil spike. It is a pattern that held through the Gulf Wars, the Arab Spring, and every major Middle East conflict of the past fifty years.

The Iran war of 2026 has torn that playbook in half.

Stocks, bonds, and gold have all declined simultaneously since February 28, 2026, with only crude oil and the US dollar posting consistent gains. Betting markets have raised the probability of a US recession in 2026 to 33%, and oil has climbed to its highest level since 2022, surging more than 40% year-to-date from its end-2025 level of approximately $60 per barrel. This post goes beyond shipping lanes and supply chains to analyze exactly what is happening — and why — in the markets that determine the cost of capital, the price of everything, and the trajectory of the global economy.

Oil Markets: The Fastest Rally Since 1983

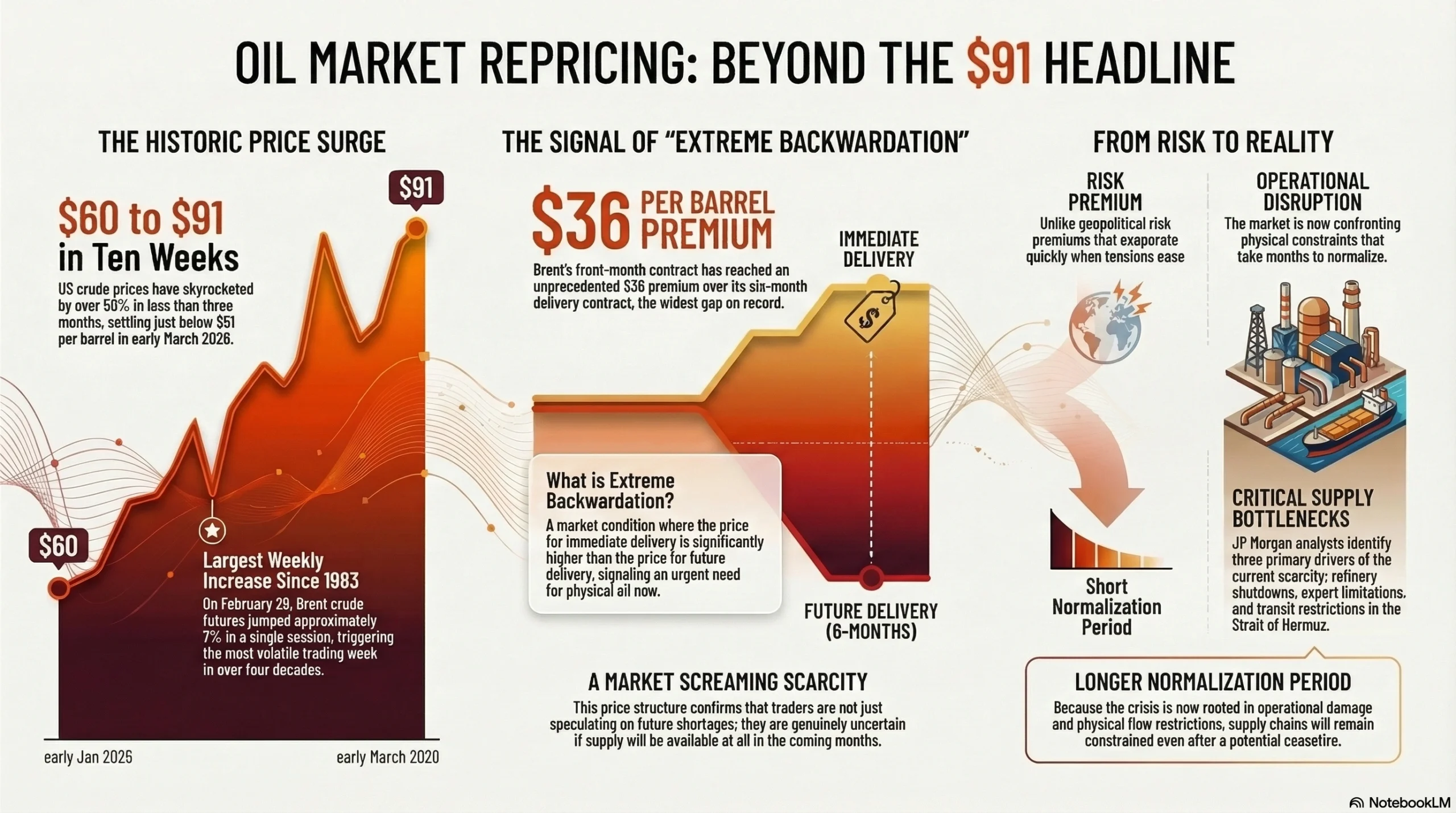

From $60 to $91 in Ten Weeks — and the Physical Market Is Even Tighter

The headline number understates the severity of the oil market repricing. US crude has settled just below $91 per barrel as of early March 2026, representing the largest single-week price increase recorded since 1983 — a move that initially saw Brent crude futures jump approximately 7% in a single trading session on February 28, before continuing to climb through the following week.

But the deeper story is in the structure of the oil market, not just the spot price. Brent’s front-month contract has reached an unprecedented premium of approximately $36 per barrel above its six-month delivery contract — a condition known as extreme backwardation. In plain terms, this means traders are paying an extraordinary premium for oil right now because they are genuinely uncertain about whether supply will be available at all over the coming months. This is not speculation about future scarcity; it is the market screaming about present scarcity.

JP Morgan analysts have highlighted the critical shift: the market is no longer merely pricing in a geopolitical risk premium — it is now confronting actual operational disruptions, as refinery shutdowns, export limitations, and Hormuz transit restrictions begin to physically constrain crude processing and supply flows. That distinction matters enormously for how long the price spike persists: risk premiums evaporate quickly when tensions ease, but operational disruptions take months to normalize even after a ceasefire.

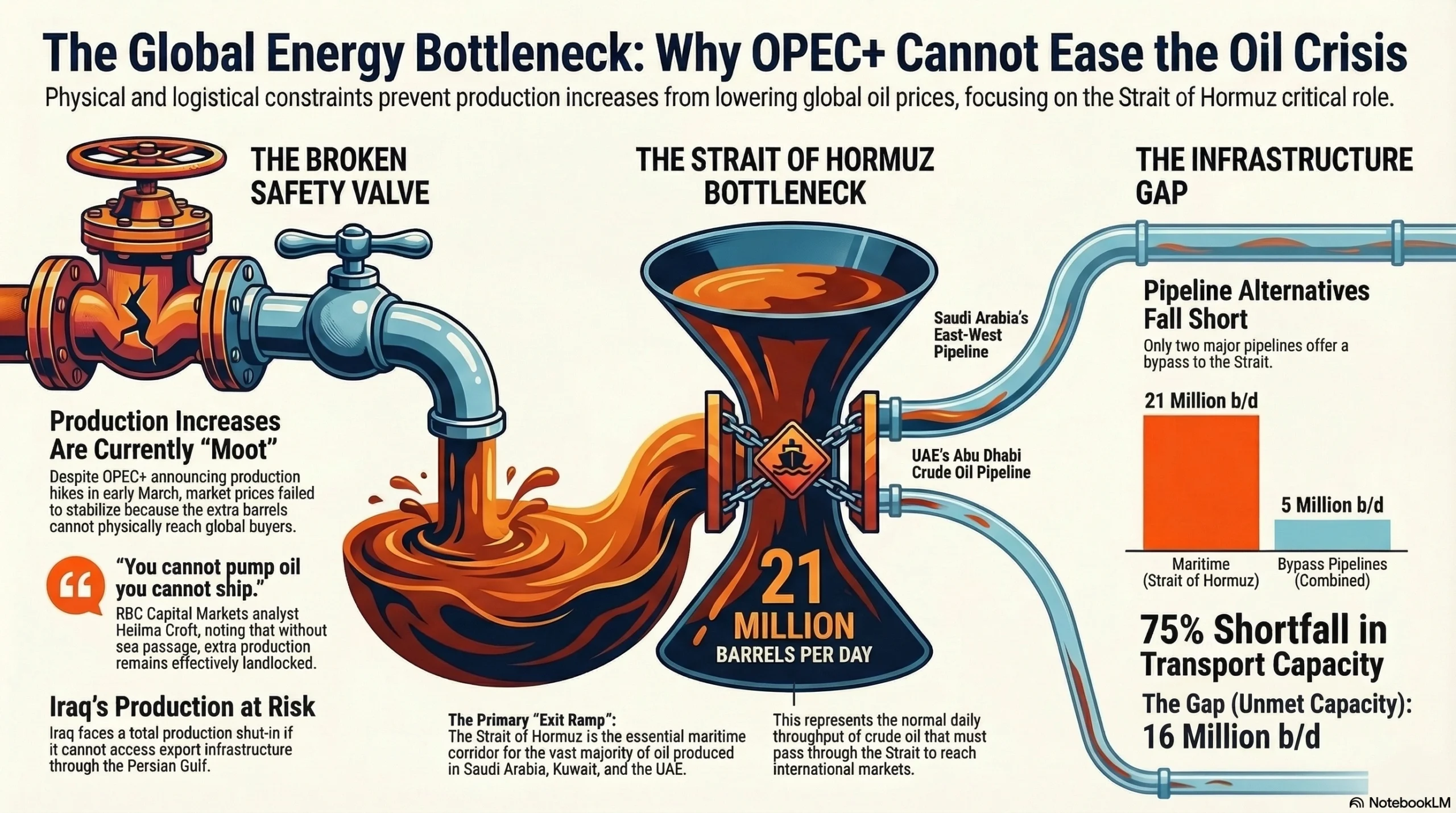

Why OPEC+ Cannot Ride to the Rescue

Every previous oil price spike of the past decade was eventually contained by the same mechanism: OPEC+ producers opening the taps to signal supply adequacy and cap the price rally. That safety valve is effectively disabled in the current crisis, for a reason that is as elegant as it is damning.

OPEC+ did announce a larger-than-expected production increase in the first week of March. The market barely reacted. RBC Capital Markets’ energy analyst Helima Croft stated the reason bluntly: “this is an entirely moot point” because of the lack of a sea passage to get those barrels to market. The Strait of Hormuz is the exit ramp for the vast majority of Gulf production. If the Strait remains closed or dangerous, extra barrels pumped in Saudi Arabia, Kuwait, or the UAE are effectively landlocked. Iraq, specifically, faces the prospect of being forced to shut in production entirely if it cannot access export infrastructure through the Gulf. You cannot pump oil you cannot ship.

The only meaningful pipeline alternatives — Saudi Arabia’s East-West Pipeline and the UAE’s Abu Dhabi Crude Oil Pipeline — have a combined maximum capacity of approximately 5 million barrels per day, against Hormuz’s normal throughput of approximately 21 million b/d. They cover less than a quarter of the gap.

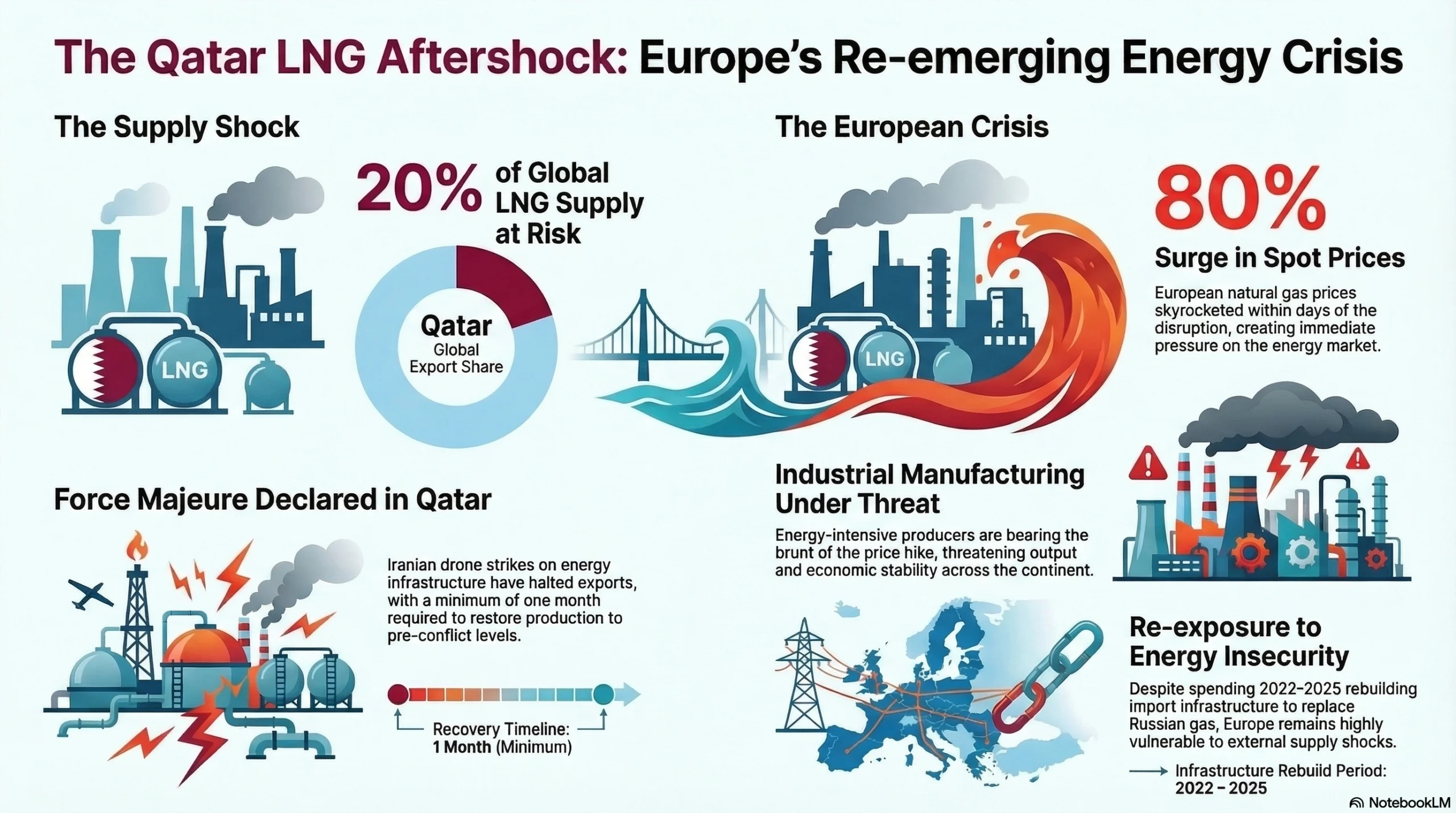

The Qatar LNG Aftershock: European Gas at Crisis Levels

Crude oil’s surge has captured most of the headlines, but a parallel shock to global natural gas markets carries equally severe economic consequences. Qatar has declared force majeure on its substantial LNG export contracts following Iranian drone strikes on its energy infrastructure, with sources indicating it may take at least a month to restore production to pre-conflict levels. Qatar contributes approximately 20% of global LNG supply — the single largest national share of any exporting country.

The consequence for European gas markets has been immediate and severe. European natural gas spot prices have surged approximately 80% in a matter of days, hitting industrial producers who rely on gas for energy-intensive manufacturing. For Europe — which spent 2022–2025 painstakingly rebuilding its LNG import infrastructure after the Russian gas cutoff — a Qatar supply disruption is a direct re-exposure to the exact energy insecurity policymakers believed was behind them.

Financial Markets: When Every Safe Haven Fails Simultaneously

The Cross-Asset Breakdown — By the Numbers

The most analytically important development since February 28 is not which assets have fallen — it is that they have all fallen together. This simultaneous decline across traditional safe-haven and risk assets has no clear modern precedent outside of the early days of the 2008 financial crisis:

| Asset Class | Direction Since Feb 28 | Key Data Point |

|---|

| Asset Class | Direction Since Feb 28 | Key Data Point |

|---|---|---|

| Brent crude | 🔴 Up sharply | +40% YTD; +30% in first week |

| WTI crude | 🔴 Up sharply | Above $80/barrel; +8% single-week gain |

| US Dollar (DXY) | 🔴 Up | Appreciating on safe-haven demand |

| S&P 500 | 🟢 Down | -0.6% on March 5 alone; negative YTD |

| Dow Jones | 🟢 Down | -400+ points on March 2 |

| Asian equities | 🟢 Down sharply | South Korea & Thailand circuit breakers triggered at -8% |

| 10-year US Treasury yield | 🟢 Rising (prices falling) | 4.13% vs 3.93% pre-conflict — equivalent to one full Fed rate hike |

| Gold | 🟢 Down | Falling despite full-scale geopolitical crisis |

| Oil major equities | 🟡 Broadly flat | Energy ETF +~2% despite 40% crude spike |

The Gold Paradox: Why the Ultimate Safe Haven Is Falling

Gold’s underperformance demands its own analysis, because it runs so contrary to historical precedent. Gold surged during the 2022 Russia-Ukraine conflict, the 2019–2020 US-Iran tensions, and effectively every major geopolitical shock in living memory. Its current decline is not a minor anomaly — it is a significant signal about what kind of crisis this actually is.

The explanation lies in the bond market. The 10-year Treasury yield has climbed from 3.93% to 4.13% since the conflict began — the equivalent of a full Federal Reserve interest rate hike compressed into days. Rising yields increase the opportunity cost of holding gold, which pays no income. When bonds offer higher yields, gold becomes relatively less attractive as a store of value. Investors are choosing to hold cash or short-duration bonds rather than gold, because this crisis is being priced as an inflation shock — not a deflation shock or a financial system stress event, which are the scenarios where gold historically performs best.

In other words, gold is not failing as a safe haven because it has lost its value. It is falling because the market has correctly identified that the primary risk here is sustained inflation driven by an energy supply shock — and cash and oil are better hedges for that specific scenario than gold.

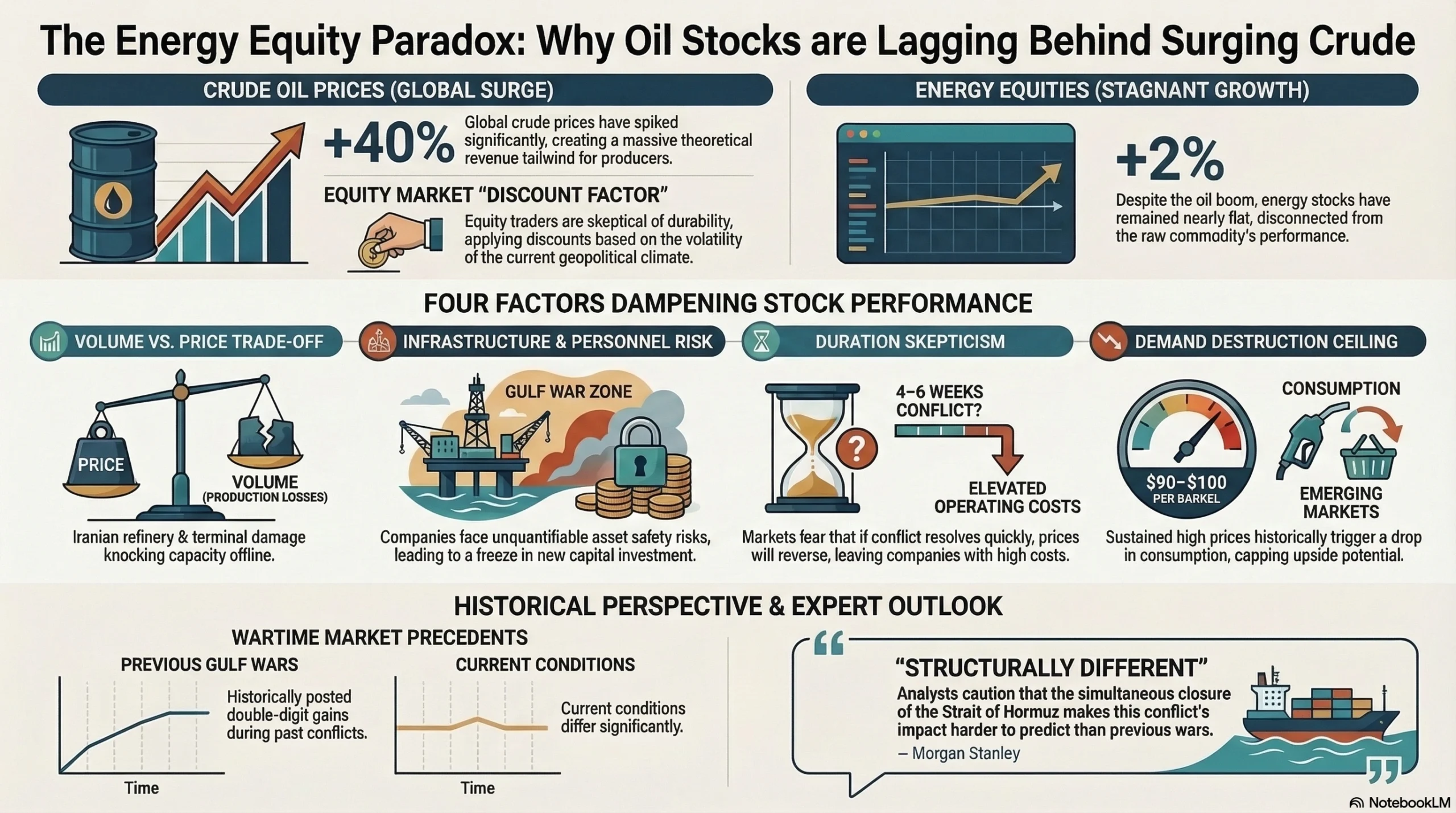

Why Oil Stocks Are Not Rallying With Oil Prices

Another counterintuitive dynamic worth examining is the near-complete disconnection between crude oil prices (up 40%) and energy company equities (up approximately 2%). Equity markets are not simply multiplying the oil price move — they are applying significant discount factors that reflect genuine uncertainty about whether the oil price spike translates into durable profitability.

Equity traders are weighing four specific negative factors against the revenue tailwind of higher crude:

Volume versus price: Higher prices are partly offset by lower volumes — Iranian refinery and terminal damage has knocked production capacity offline, so some of the region’s oil is not being sold at any price

Infrastructure and personnel risk: Oil majors with Gulf exposure face asset safety risks that are not yet fully quantifiable; no company will accelerate capital investment in a war zone

Duration skepticism: If the conflict resolves in four to six weeks, the oil spike reverses sharply — and companies that lock in operating cost assumptions at elevated levels face a painful adjustment

Demand destruction ceiling: Sustained oil prices above $90–100 per barrel historically trigger demand destruction in price-sensitive emerging markets, capping the theoretical upside and potentially creating an inventory glut if supply resumes suddenly

Morgan Stanley analysts advise investors to note that markets have historically posted gains during wartime — including double-digit increases during both Gulf Wars — but caution that this conflict’s duration and the simultaneous Hormuz closure make it structurally different from those precedents.

Bond Markets and the Inflation Signal

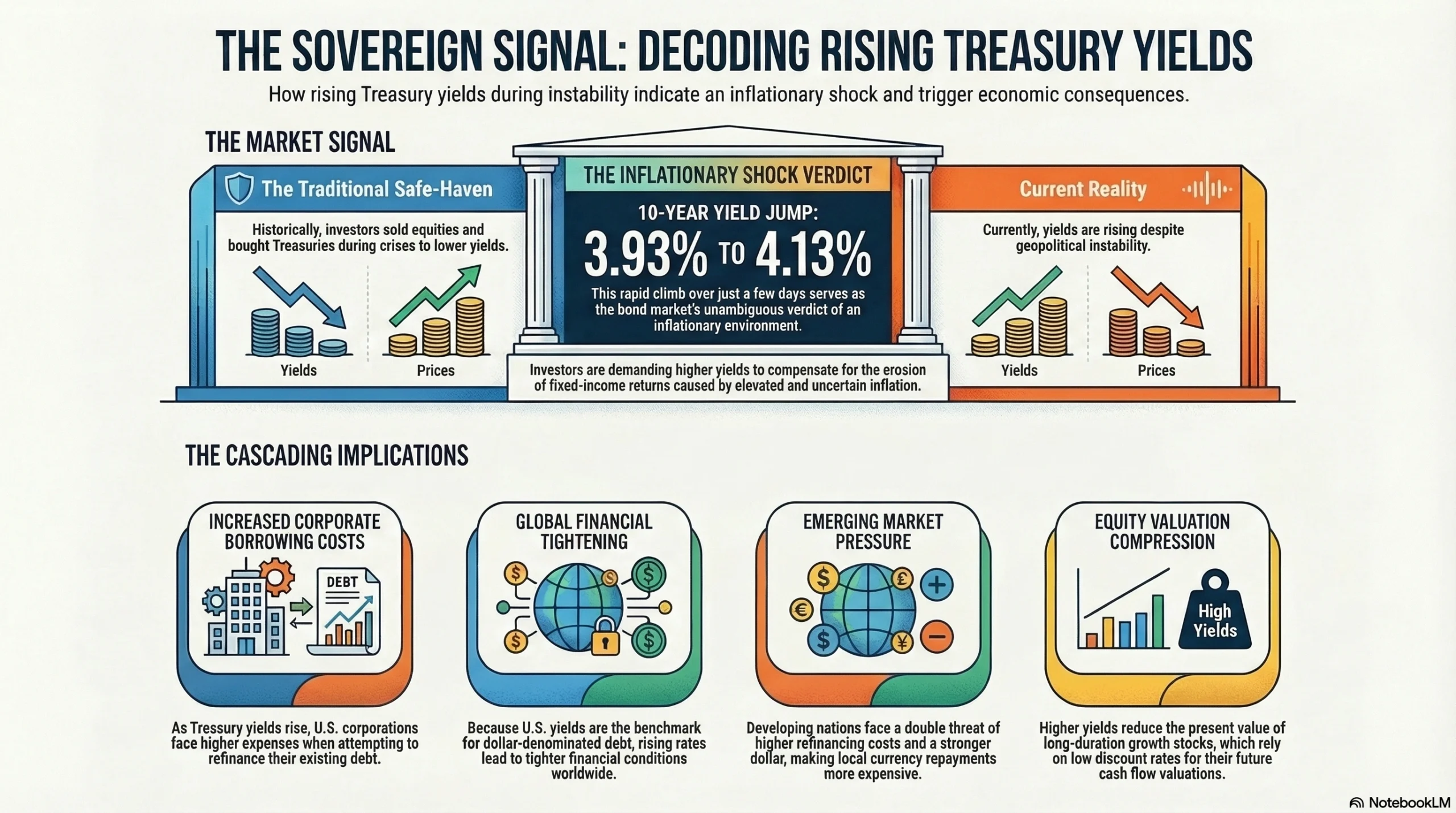

US Treasury bonds are supposed to be the world’s premier safe-haven asset. In every major crisis of the past quarter century, investors have sold equities and bought Treasuries, pushing yields down and prices up. The fact that yields are rising — bond prices falling — during a full-scale geopolitical crisis is one of the most important signals in current markets, and it deserves far more attention than it is receiving in mainstream financial coverage.

The 10-year Treasury yield climbing from 3.93% to 4.13% in days is the bond market’s unambiguous verdict: this is an inflationary shock, not a deflationary one. Bond investors are not buying Treasuries for safety because they are more worried about inflation eroding the real value of their fixed-income returns than they are about equity market losses. They are demanding higher yields as compensation for an environment of elevated and uncertain inflation.

This has cascading implications. Rising Treasury yields mean:

Higher borrowing costs for US corporations refinancing debt

Tighter financial conditions globally, since US yields set the benchmark for dollar-denominated debt worldwide

Pressure on emerging market sovereigns that have borrowed heavily in dollars and now face both higher refinancing costs and a stronger dollar making repayment more expensive in local currency terms

Reduced present value of long-duration equity valuations — particularly relevant for growth stocks whose valuations depend on discounting future cash flows at lower rates

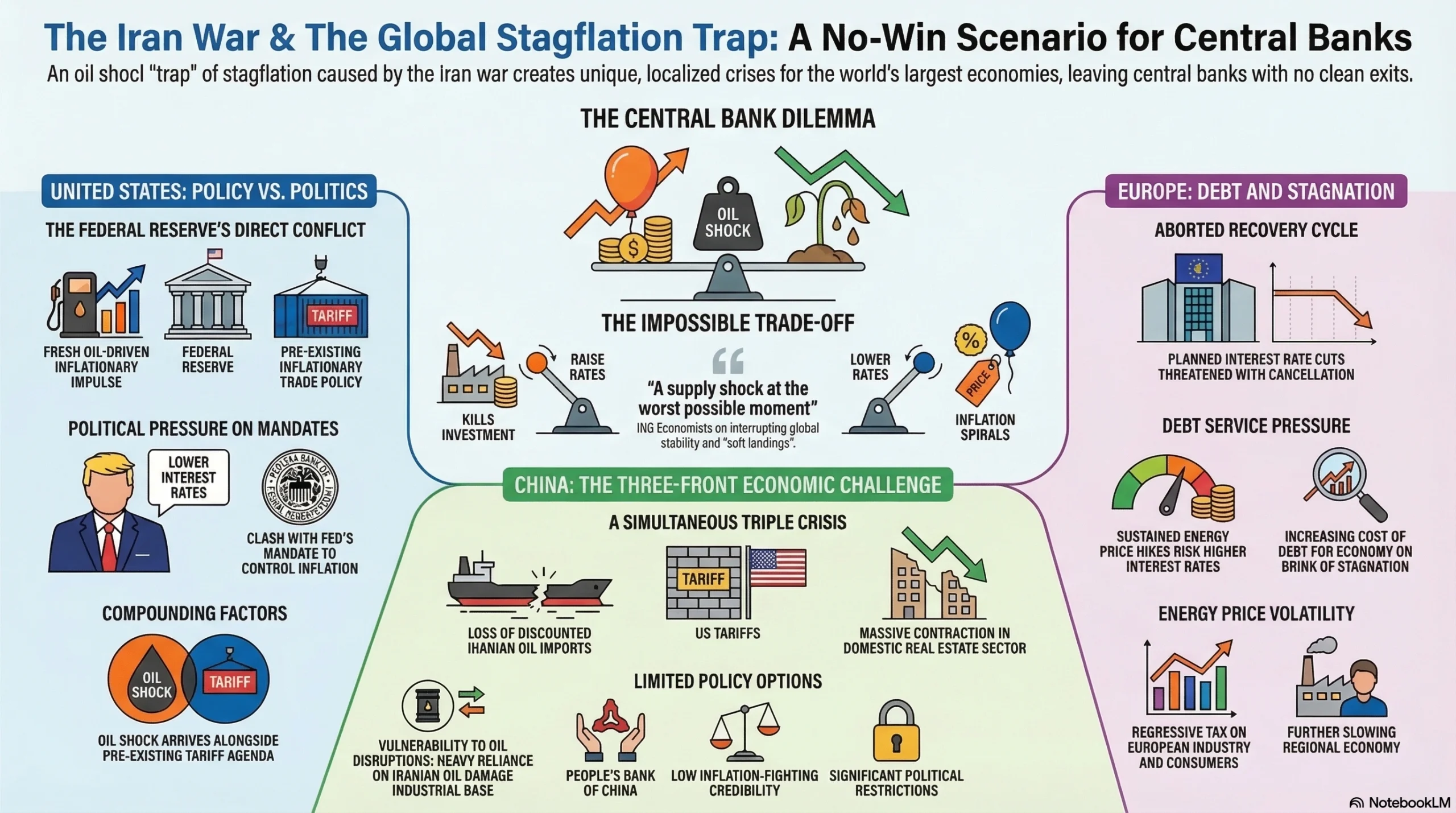

The Central Bank Dilemma: Stagflation's Return

The Iran war has handed central banks around the world an extraordinarily difficult macroeconomic puzzle. The situation mechanically resembles the 1973–1974 Arab oil embargo stagflation crisis, but with a far more complex and interconnected global financial system layered on top.

The dilemma is structural and inescapable: an oil shock simultaneously pushes inflation up and growth down. Raising rates to fight inflation suppresses the investment and consumption needed to sustain growth. Cutting or holding rates to protect growth allows inflation to entrench. There is no clean exit from this trap — every move is a trade-off.

For the US Federal Reserve, the energy shock pushes inflation higher while President Trump simultaneously demands lower interest rates — placing the Fed in a direct conflict between its inflation mandate and significant political pressure. The Iran war is the latest compounding threat to a global economy already rattled by Trump’s tariff agenda, meaning the Fed must navigate a fresh oil-driven inflationary impulse while the underlying trade policy environment is itself already inflationary.

For China, the loss of discounted Iranian oil imports lands on top of Trump’s tariffs and an ongoing real estate sector contraction — a simultaneous three-front economic challenge with no obvious policy solution. The People’s Bank of China faces the same structural dilemma in an economy with even less inflation-fighting credibility and more politically constrained options.

For Europe, sustained higher energy prices risk driving inflation back up and, with it, interest rates — adding debt service pressure across an economy already near stagnation. The European Central Bank had been approaching its first genuine rate-cutting cycle in years. That cycle is now under threat of being aborted before it generates meaningful economic relief.

ING economists summarized the situation with precision: the Iran war is “a supply shock at the worst possible moment” — arriving precisely when major economies were closest to achieving soft landings after three years of aggressive monetary tightening. The timing transforms what might have been a manageable disruption into a genuine macro-level risk event.

Currency Markets: Dollar Dominance Reasserted — For Now

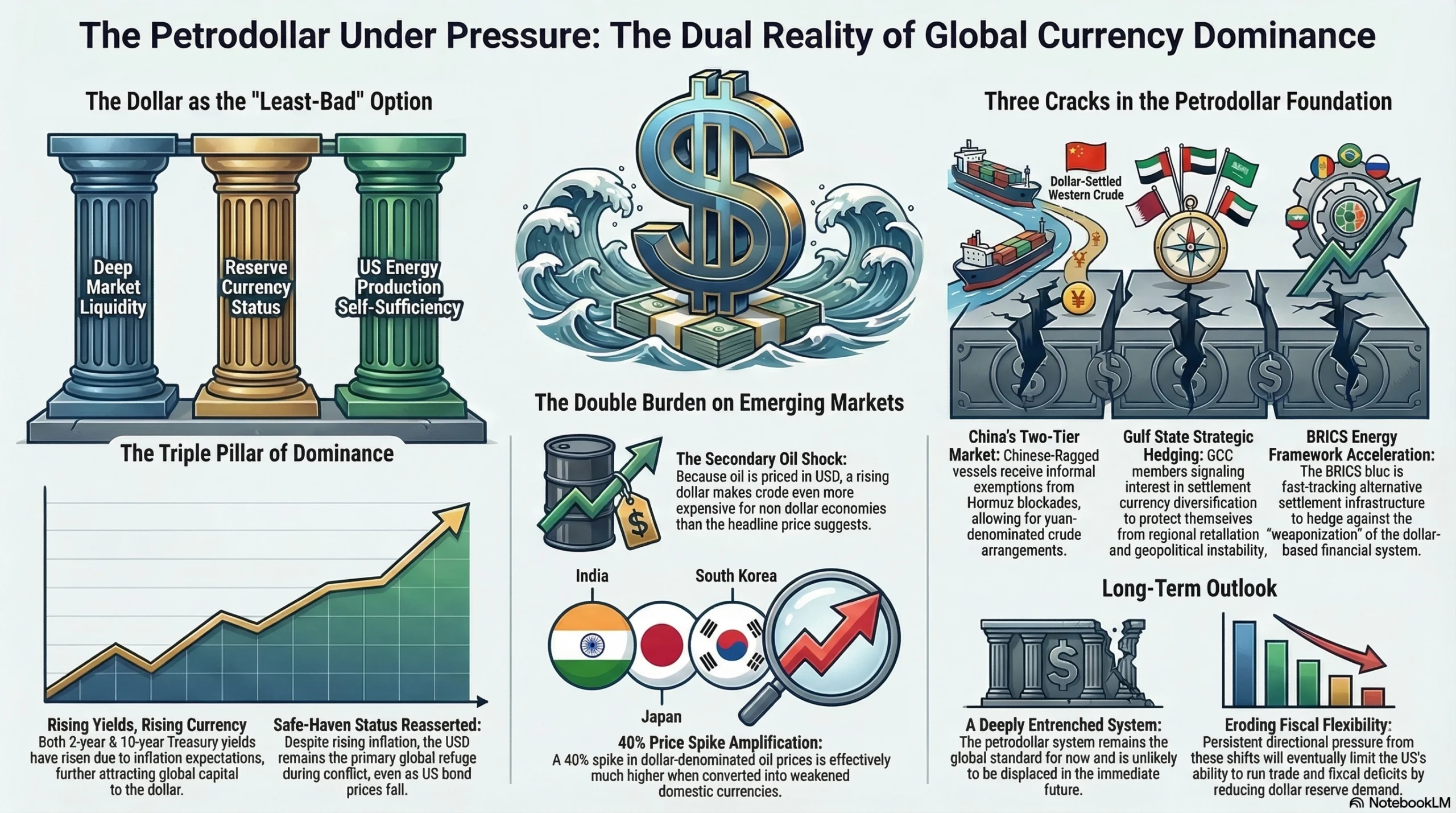

The Dollar as the Crisis Beneficiary

The US dollar has appreciated since the conflict began, with both 2-year and 10-year Treasury yields rising partly due to heightened inflation expectations — reinforcing the dollar’s reserve currency safe-haven role even as US bond prices fall. This creates an important dynamic: the dollar is rising not because US assets are seen as safe, but because in a world where every major currency faces an energy-driven inflation shock, the dollar’s structural advantages — deep liquidity, reserve currency status, energy production self-sufficiency — make it the least-bad option.

Dollar appreciation, however, creates a painful secondary effect for the global economy. Oil is priced in dollars. When the dollar rises, the real cost of oil for non-dollar economies rises even more than the headline crude price suggests. A country like India, Japan, or South Korea that was already absorbing a 40% oil price spike in dollar terms is now absorbing an even larger increase in domestic currency terms after accounting for local currency depreciation against the dollar. This secondary channel of the oil shock is often overlooked but is economically significant, particularly for energy-import-dependent emerging markets.

The Petrodollar System Under Stress

A deeper geopolitical financial dynamic that deserves analytical attention is the subtle but real stress this conflict is placing on the petrodollar system — the foundational arrangement under which Gulf oil is priced in US dollars, underpinning global dollar demand and the US’s structural ability to run persistent trade and fiscal deficits.

The Iran war is complicating this architecture in three ways simultaneously:

China’s informal Hormuz exemption — Vessel-tracking data shows Chinese-flagged vessels appearing to receive informal exemptions from Iran’s de facto Hormuz blockade, effectively creating a two-tier oil market: dollar-settled Western crude and yuan-denominated Chinese crude arrangements

Gulf state currency diversification signaling — Gulf Cooperation Council members caught between Iranian retaliation and US military presence are signaling interest in settlement currency diversification as a strategic hedge, chipping incrementally at the exclusivity of dollar-denominated energy trade

BRICS energy framework acceleration — The alternative cross-border settlement infrastructure already under construction within the BRICS bloc gains renewed strategic urgency and political momentum as a hedge against dependence on a dollar system that is increasingly weaponized in geopolitical conflicts

None of these trends will displace the petrodollar system in the near term — it is deeply entrenched — but they represent the directional pressure that a prolonged conflict accelerates, with long-term implications for dollar reserve demand and US fiscal flexibility.

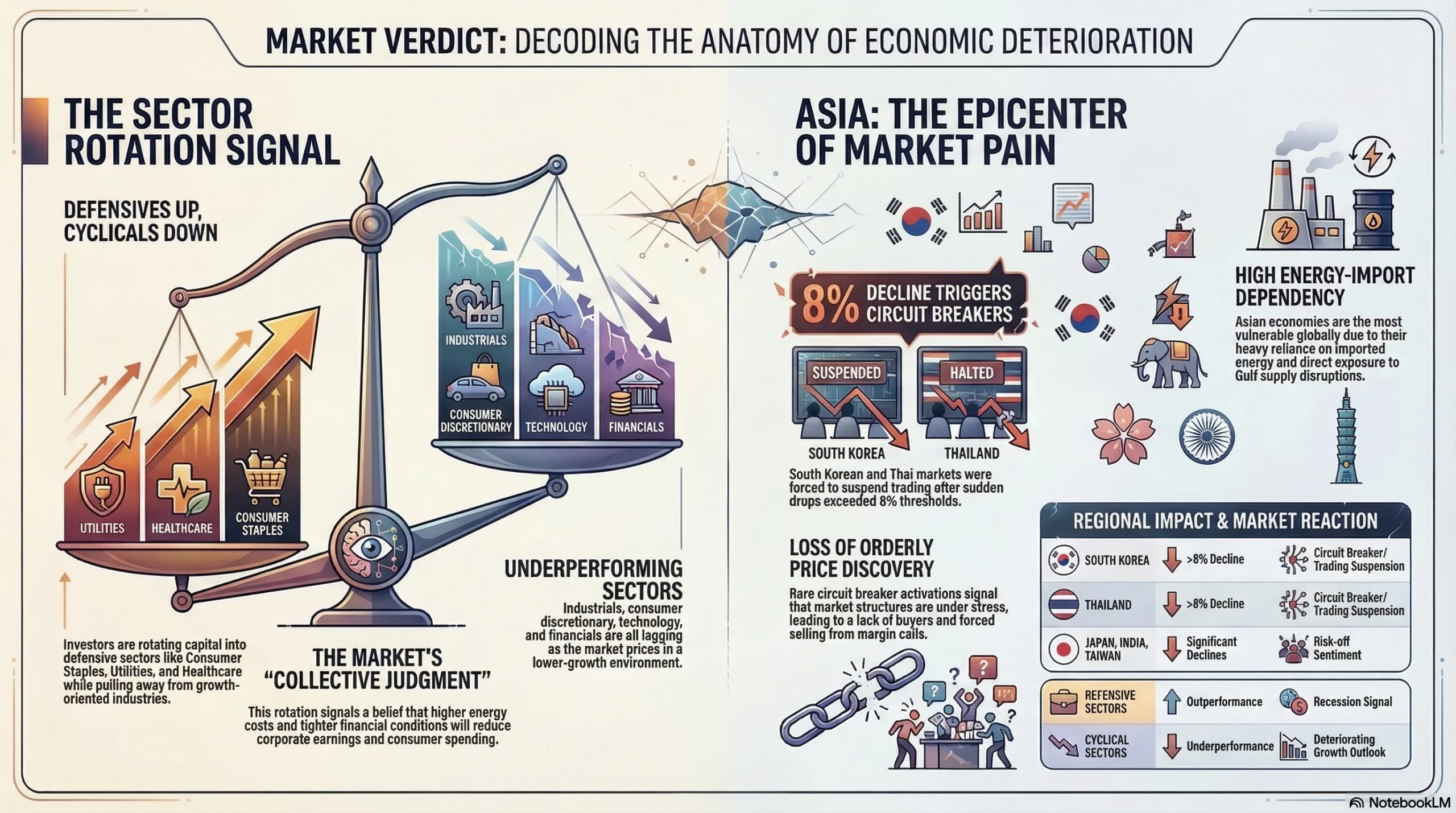

Sector Rotation: Reading the Market's Verdict on the Economy

Defensives Up, Cyclicals Down — The Recession Signal

Within equity markets, a clear and economically meaningful sector rotation is underway that serves as a live barometer of investor confidence in the growth outlook. Defensive stocks — those less sensitive to economic fluctuations, such as consumer staples, utilities, and healthcare — have outperformed cyclical sectors since the conflict began. Industrials, consumer discretionary, technology, and financials are all underperforming.

This rotation is not a random investor preference. It is a collective judgment that economic growth is deteriorating — that higher energy costs, tighter financial conditions, and policy uncertainty will reduce corporate earnings and consumer spending over the coming quarters. When money flows from growth stocks to staples and utilities, it is the market pricing in a lower-growth or recessionary environment.

Asian Equity Markets: The Epicentre of Pain

The most severe equity market reactions globally have occurred in Asia, for economically straightforward reasons: Asian economies are the most energy-import-dependent and carry the heaviest direct exposure to Gulf supply disruptions. South Korean and Thai stock markets were forced to suspend trading after dropping more than 8%, activating circuit breakers designed to prevent panic selling. Japan, India, and Taiwan also saw significant declines reflecting both direct energy cost exposure and the broader risk-off sentiment.

The circuit breaker activations are particularly significant because they are relatively rare events — they signal not just a market decline but a loss of orderly price discovery. When buyers step back entirely, market structure itself comes under stress, and the resulting forced selling from margin calls and risk management systems can amplify the initial shock well beyond what economic fundamentals alone would justify.

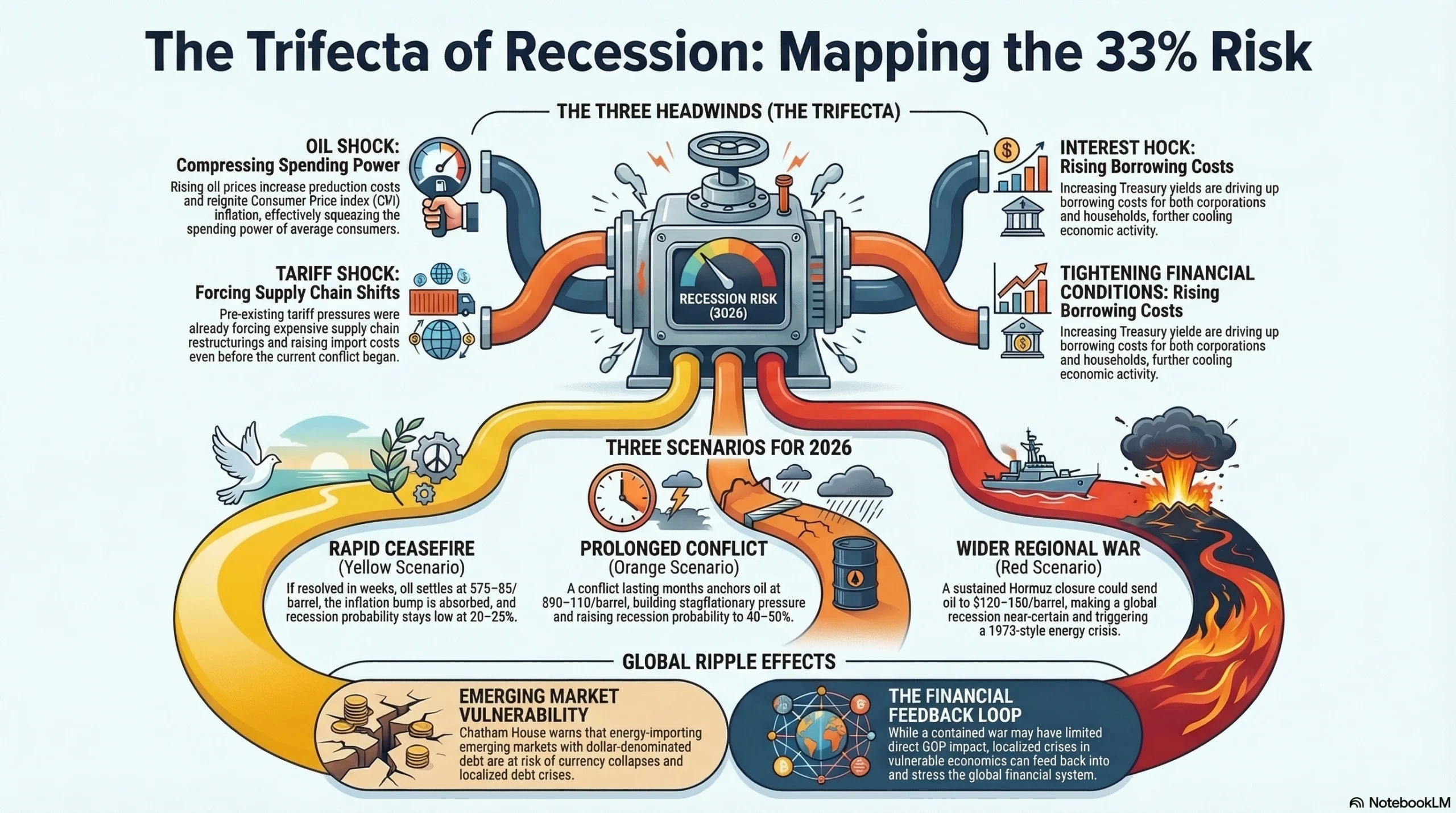

Recession Risk: The 33% Probability and What Drives It Higher

Betting markets have raised the likelihood of a US recession in 2026 to 33% since the conflict began — a significant shift from the 15–18% range that prevailed before February 28. This figure is not generated arbitrarily; it reflects the compounding logic of three simultaneous economic headwinds:

| Headwind | Channel of Economic Damage |

|---|

| Headwind | Channel of Economic Damage |

|---|---|

| Oil shock | Raises production costs, compresses consumer spending power, reignites CPI |

| Tariff shock | Already forcing supply chain restructuring and raising import costs before the conflict |

| Financial conditions tightening | Rising Treasury yields increase borrowing costs for corporations and households |

🟡 Rapid ceasefire (weeks): Oil settles at $75–85/barrel. Inflation bump is absorbed. Soft landing preserved. Recession probability stays around 20–25%

🟠 Prolonged conflict (months): Oil anchors at $90–110/barrel. Stagflationary pressure builds. Recession probability rises to 40–50%. Central banks paralyzed by the inflation-growth trade-off

🔴 Wider regional war / sustained Hormuz closure: Oil surges to $120–150/barrel. Global recession near-certain. 1973-style energy crisis. Sovereign debt stress in energy-importing emerging markets with dollar-denominated liabilities

Chatham House economists offer a partial counterpoint, assessing that even a long war would have limited direct consequences for global GDP if it remains contained to its current scope — but critically add that “some emerging economies are vulnerable to persistent high energy prices” in ways that could trigger localized debt crises and currency collapses that then feed back into global financial stress.

What Investors and Finance Professionals Should Do Now

Based on the current market dynamics and the analysis from Morgan Stanley, JP Morgan, RBC Capital Markets, and ING, the following strategic implications stand out for portfolios, treasury functions, and corporate finance teams:

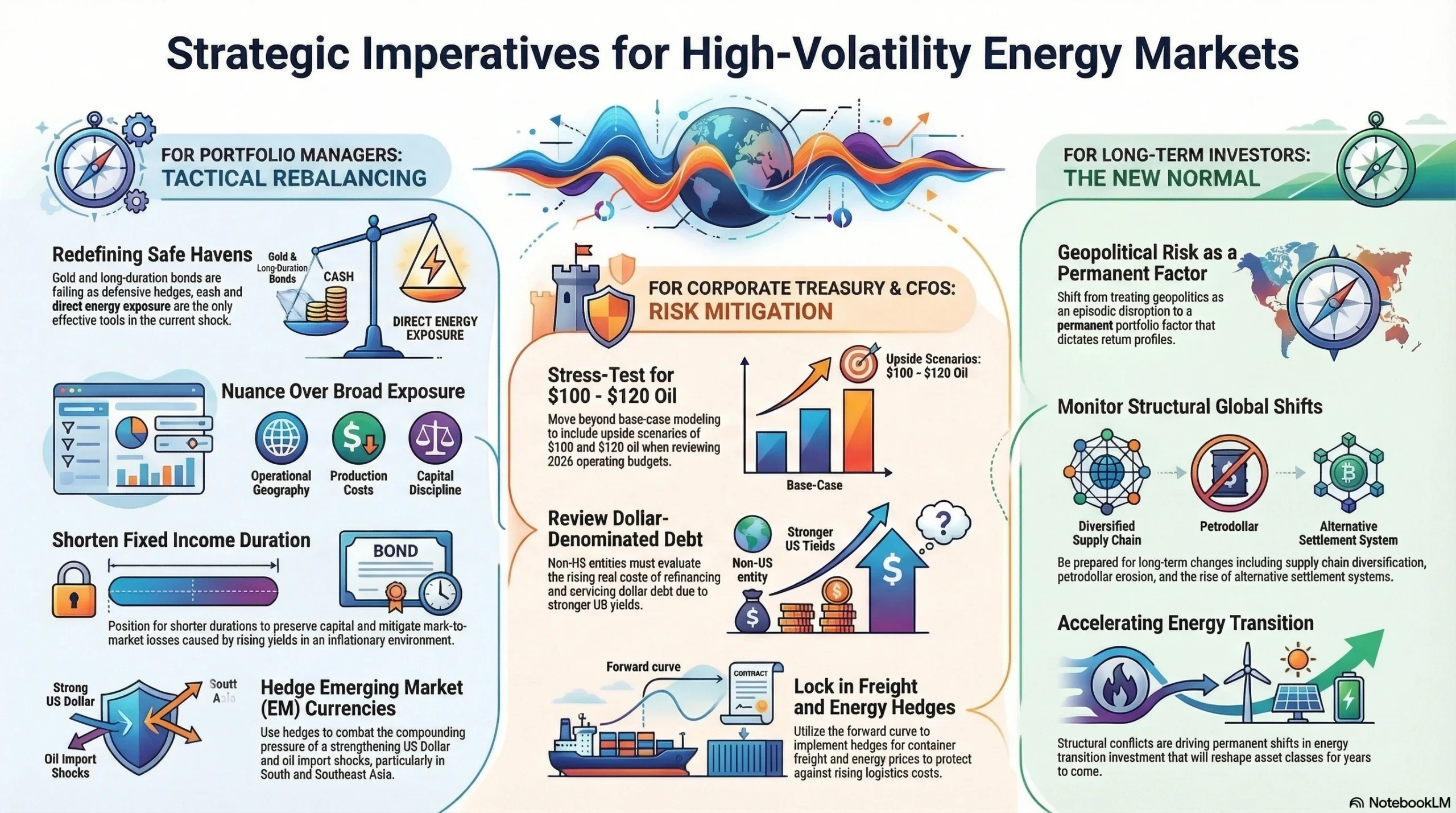

For Portfolio Managers:

Reassess safe-haven assumptions — Gold and long-duration bonds are not functioning as traditional defensive hedges in this specific shock; cash and energy exposure are the actual effective hedges right now

Apply nuance to energy equities — The crude price surge is not translating cleanly into energy stock gains; selective exposure based on operational geography, production costs, and capital discipline is warranted, not broad-brush energy sector buying

Shorten fixed income duration — Rising yields in an inflationary shock environment create mark-to-market losses for long-duration bondholders; shorter-duration positioning preserves capital more effectively

Hedge emerging market currency exposure — Dollar appreciation combined with an oil import shock creates compounding pressure on EM currencies, particularly in South and Southeast Asia

For Corporate Treasury and CFO Teams:

Stress-test at $100 and $120 oil — The current environment warrants modeling two upside scenarios, not just a base case; energy cost assumptions embedded in 2026 operating budgets need urgent review

Review dollar-denominated debt exposure — Rising US yields and a stronger dollar increase the real cost of refinancing and servicing dollar debt for non-US entities

Implement freight and energy hedging — Demand for container freight futures and energy price hedges is surging; the forward curve offers meaningful protection for companies with significant logistics or energy cost exposure

For Long-Term Investors:

Treat geopolitical risk as a permanent portfolio factor, not an episodic disruption. The structural changes this conflict is accelerating — supply chain diversification, energy transition investment, petrodollar erosion, alternative settlement systems — will reshape return profiles across multiple asset classes for years, not months

Conclusion: The Market Verdict Is In — This Is a Structural Shift

The Iran war’s financial and trading fallout is not a temporary market dislocation that will reverse when a ceasefire is signed. It has exposed three structural vulnerabilities in the global financial system that predate the conflict but have been brought into sharp, undeniable focus by it.

The three structural conclusions that financial decision-makers cannot ignore:

The safe-haven playbook is broken for supply shock scenarios. When the primary risk is inflation rather than deflation or financial system stress, the traditional crisis rotation — stocks out, bonds and gold in — does not work. The market is telling you that directly, in real time, with observable price data

Oil market structure has changed fundamentally. The extreme backwardation in crude futures, the OPEC+ capacity ceiling, and the Hormuz geography trap together mean that the historical assumption — that oil spikes are self-correcting because supply can always be increased — is no longer reliably true

Stagflation is the realistic base case, not a tail risk. The combination of an oil supply shock, ongoing tariff-driven trade cost inflation, and rising financing costs has created the precise economic conditions for stagflation — and central banks have no clean policy tool to fight it without causing collateral damage

The businesses, funds, and policymakers that navigate this era best will be those that resist the urge to wait for normalcy to return and instead build their strategies around the world as it actually is: one where geopolitical risk is a permanent pricing factor, energy security is a first-order strategic priority, and the assumption that global supply chains will remain efficient and uninterrupted has been permanently retired.

FAQs

US-Israel strikes on Iran triggered immediate Hormuz Strait disruptions, physically blocking approximately 20% of global oil supply with no detour available. Combined with OPEC+’s inability to reroute stranded Gulf barrels, the market is pricing real operational supply loss — not just geopolitical fear — pushing Brent above $91/barrel.

Because this is an inflation shock, not a financial crisis. Traditional safe havens like bonds and gold lose appeal when rising energy prices drive inflation higher. Investors are holding cash and crude instead — breaking the conventional crisis playbook that portfolio managers have relied on for decades.

It creates a stagflationary trap. Higher oil prices push inflation up while simultaneously slowing growth — leaving the Fed unable to cut rates without worsening inflation, or raise rates without deepening the economic slowdown. Betting markets have already raised US recession probability to 33% in 2026.

Equity markets are discounting four risks: lower production volumes from damaged Iranian infrastructure, uncertain conflict duration, potential demand destruction above $90/barrel, and Gulf asset safety concerns. The iShares Global Energy ETF has risen only ~2% despite crude surging 40% year-to-date.

The dollar is appreciating as the relative safe-haven currency, making oil — priced in dollars — even more expensive for emerging economies. Nations like India, South Korea, and Turkey face a double hit: surging crude prices compounded by local currency depreciation, sharply raising real energy import costs.

Not inevitable, but increasingly probable. A rapid ceasefire keeps recession risk around 20–25%. A prolonged conflict with oil at $90–110/barrel pushes that probability to 40–50%. A full Hormuz closure sustained for months would make global recession near-certain, according to JP Morgan and ING economists.