The Cost Nobody Sees

When consumers see prices rising at the supermarket, at the pump, or on a shipping invoice, they blame oil prices, tariffs, or “the war.” Almost nobody blames insurance — and that’s precisely why it’s the most powerful hidden force in global trade right now.

The war-risk insurance market — a centuries-old, obscure corner of global finance — has become the single largest invisible cost multiplier in 2026’s trade disruption. Premium increases of 1,000% or more are cascading through every product that touches a ship, a port, or a trade lane connected to the Middle East. The Strait of Hormuz, already the world’s most critical energy chokepoint, has now become what industry experts are calling the world’s most expensive waterway. And yet, this systemic shock rarely makes the front page.

This article explains exactly how that system works, why it’s breaking, and what it means for every business on Earth. By the time you finish reading, you’ll understand:

How war-risk insurance actually works — demystified for non-specialists

What’s happening right now in the market — with hard data and a real-time premium timeline

How these costs reach your invoice, your shelf price, your margin

How 2026 compares to previous Gulf conflicts — from the 1980s Tanker War to the 2024 Houthi attacks

Why the U.S. government took the unprecedented step of entering the insurance market

What your business should do right now

The war-risk insurance crisis isn’t a footnote to the Hormuz conflict. It is the Hormuz conflict — playing out on balance sheets, freight invoices, and eventually, in every aisle of every store.

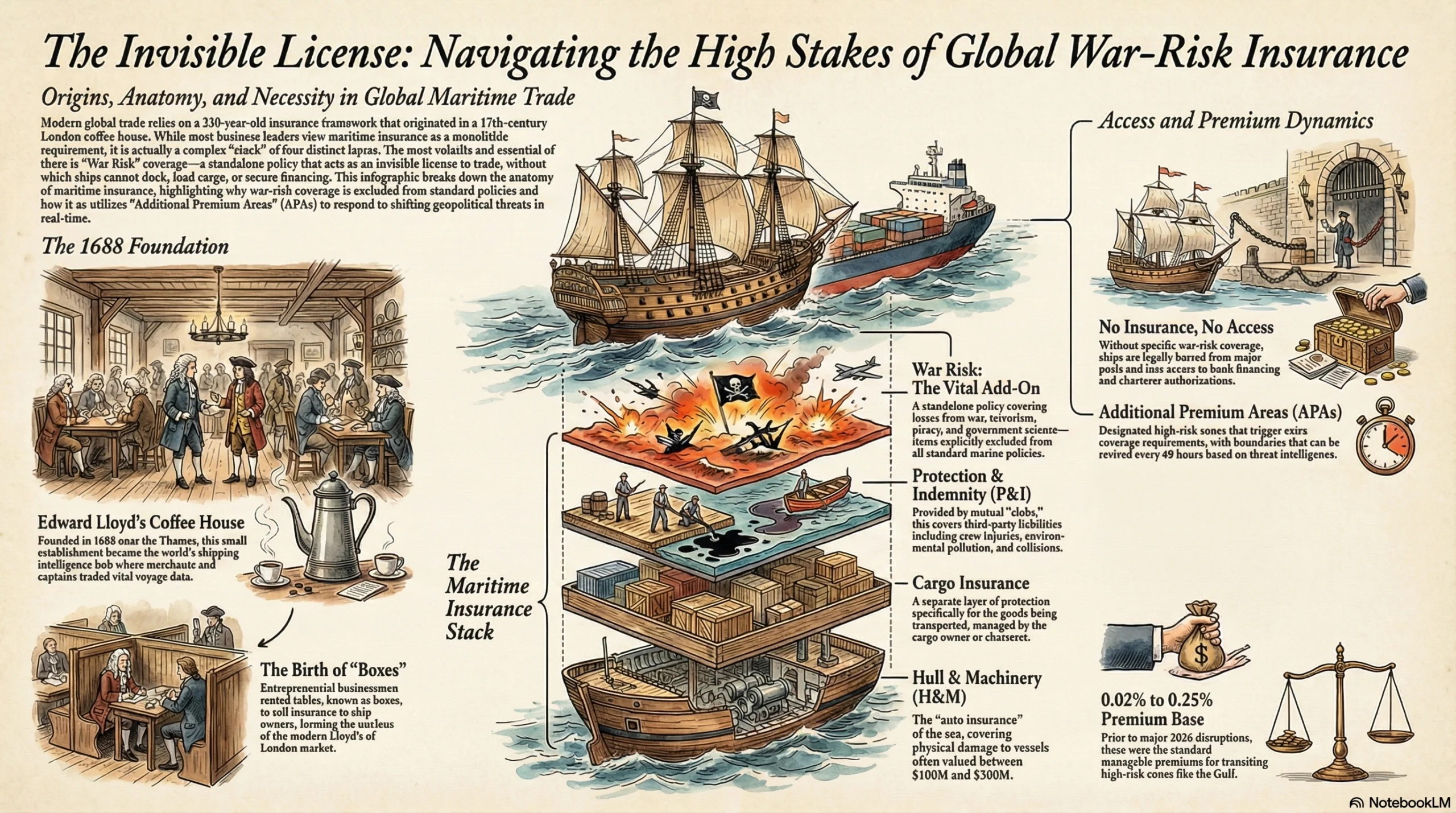

A 330-Year-Old System You've Never Heard Of

To understand how war-risk insurance is disrupting global trade in 2026, you first need to understand what it is — and why it exists at all.

The story begins in 1688 at Edward Lloyd’s Coffee House in London, a small establishment near the Thames where merchants, ship captains, and financiers gathered to trade information about voyages. Lloyd’s coffee house specialized in shipping intelligence, and it didn’t take long before entrepreneurial businessmen began renting out the tables — called “boxes” — to sell insurance to ship owners who feared their vessels might not return from sea. That informal marketplace became the nucleus of what is now Lloyd’s of London, the world’s most important specialist insurance market, and the backbone of global maritime risk coverage to this day.

The insurance “stack” every ship carries is more complex than most business leaders realize. A modern commercial vessel typically holds four layers of coverage:

Hull & Machinery (H&M): Covers physical damage to the ship itself — the equivalent of auto insurance for a vessel worth $100M to $300M or more.

Cargo Insurance: Covers the goods being transported — managed separately by the cargo owner or charterer.

Protection & Indemnity (P&I): Third-party liability coverage, typically provided by mutual P&I Clubs, covering crew injury, pollution, cargo damage claims, and collision liability.

War Risk: A standalone add-on that covers losses caused by war, terrorism, piracy, mines, hostile acts, and government seizure.

That last layer is critical — and critically misunderstood. War risk is explicitly excluded from every standard marine policy. It is not bundled in. It must be purchased separately, from a separate market, under separate policy wording. Without it, the consequences are total: ships cannot legally dock at most major ports, charterers will not authorize cargo loading, and banks will not finance the voyage.

War-risk insurance is, functionally, the invisible license to trade.

The market operates through what are called “Additional Premium Areas” (APAs) — designated high-risk zones that trigger extra coverage requirements. These designations can be revised every 48 hours to seven days, depending on the severity of threat intelligence. Before February 28, 2026, normal war-risk premiums for a Gulf transit were a modest 0.02% to 0.25% of a vessel’s hull value — a manageable cost, barely noticed in most shipping budgets. What happened next was anything but manageable.

What Happened When the Strait Closed

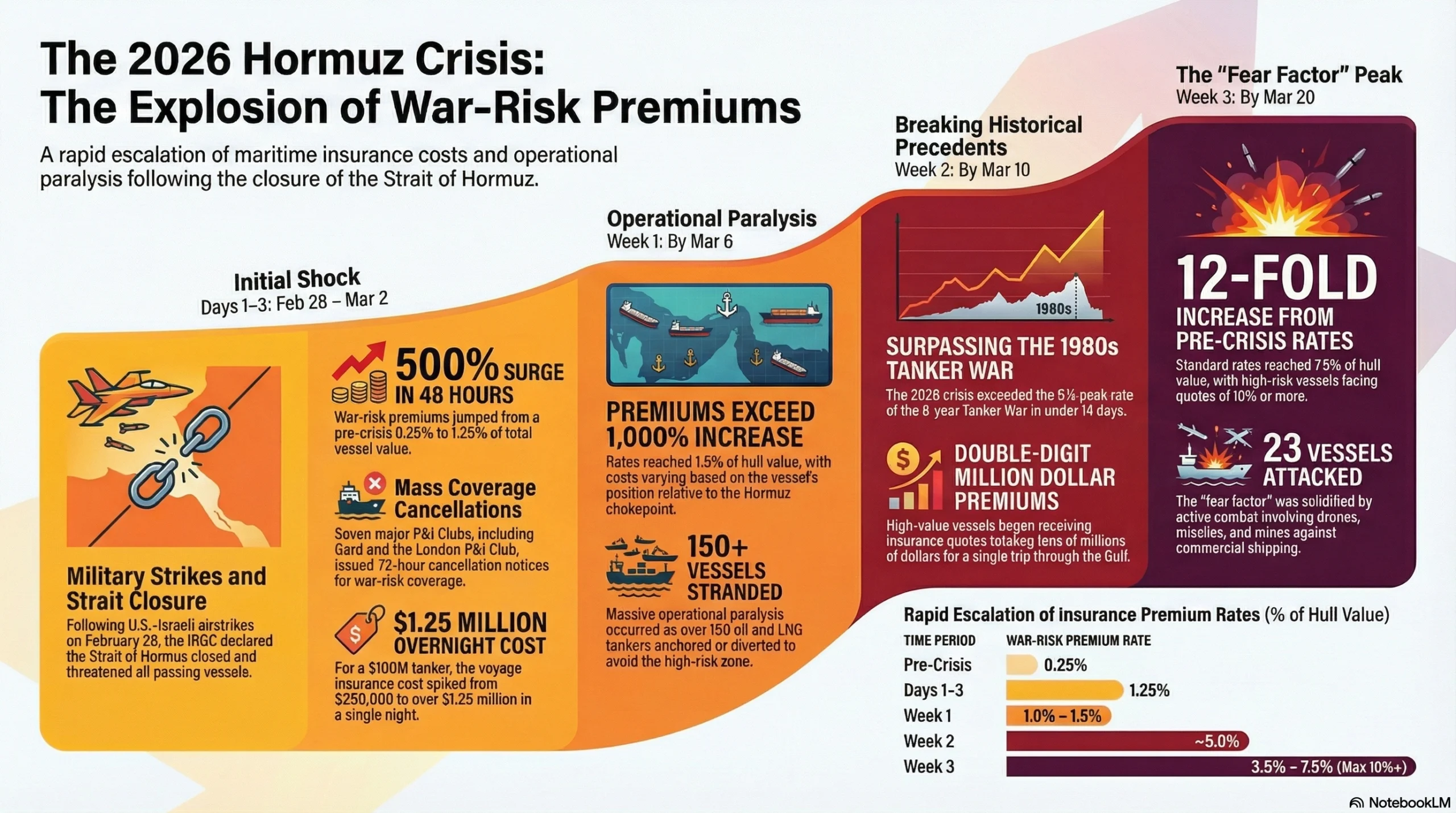

The timeline of the 2026 war-risk premium explosion is one of the most dramatic in modern financial history — and it unfolded not over months, but over days.

Day 1–3 (Feb 28 – Mar 2, 2026): Within 48 hours of coordinated U.S.–Israeli airstrikes on Iran on February 28, war-risk premiums surged fivefold. Iran’s Islamic Revolutionary Guard Corps (IRGC) declared the Strait of Hormuz “closed” and threatened to strike any vessel attempting passage. At least seven major P&I Clubs — including Gard, Skuld, NorthStandard, the London P&I Club, and the American Club — issued 72-hour cancellation notices for war-risk coverage across the Gulf. Marsh Risk reported that rates had already jumped from 0.25% to 1.25% of vessel value within the first 48 hours. For a $100M tanker, that’s a voyage cost that went from roughly $250,000 to over $1.25 million — overnight.

By Week 1 (Mar 6): Reuters reported surges exceeding 1,000%. Marsh’s marine hull UK war leader Dylan Mortimer confirmed that rates were generally ranging from 1% to 1.5% of hull value, with further variation depending on whether a vessel was positioned east or west of the Hormuz chokepoint. Over 150 vessels, including oil and LNG tankers, had anchored or diverted, creating immediate operational paralysis.

By Week 2 (Mar 10): Lloyd’s List reported that Gulf war-risk premiums were topping double-digit millions of dollars per trip for high-value vessels. For context, the typical rate during the 1980s Tanker War — when Iraq attacked 283 vessels and Iran attacked 168 over eight years — was approximately 5%. The 2026 crisis had blown past that precedent in under two weeks.

By Week 3 (Mar 20): Commercial Risk Online confirmed that war-risk rates for ships in Gulf waters had reached 3.5% to 7.5% of hull value per voyage, with some high-risk vessels facing quotes at 10% or more. The Financial Times reported that in some cases premiums had increased twelvefold from pre-crisis rates. By this point, 23 vessels had been attacked, involving drones, missiles, mines, and direct naval exchanges — contributing to what insurers were calling an unprecedented “fear factor.”

The following table illustrates the premium trajectory over the first three weeks of the crisis:

| Date | Premium (% of hull value) | Cost for $100M tanker (single trip) |

|---|---|---|

| Pre-war (before Feb 28) | 0.02–0.25% | $20K–$250K |

| Day 3 (Mar 2) | ~1–1.25% | ~$1M–$1.25M |

| Week 1 (Mar 6) | 1–1.5% | $1M–$1.5M |

| Week 2 (Mar 10) | 1.5–3% | $1.5M–$3M |

| Week 3 (Mar 20) | 3.5–7.5% | $3.5M–$7.5M |

| High-risk vessels | Up to 10%+ | $10M+ |

History Repeats, But Louder: War-Risk Insurance in Past Conflicts

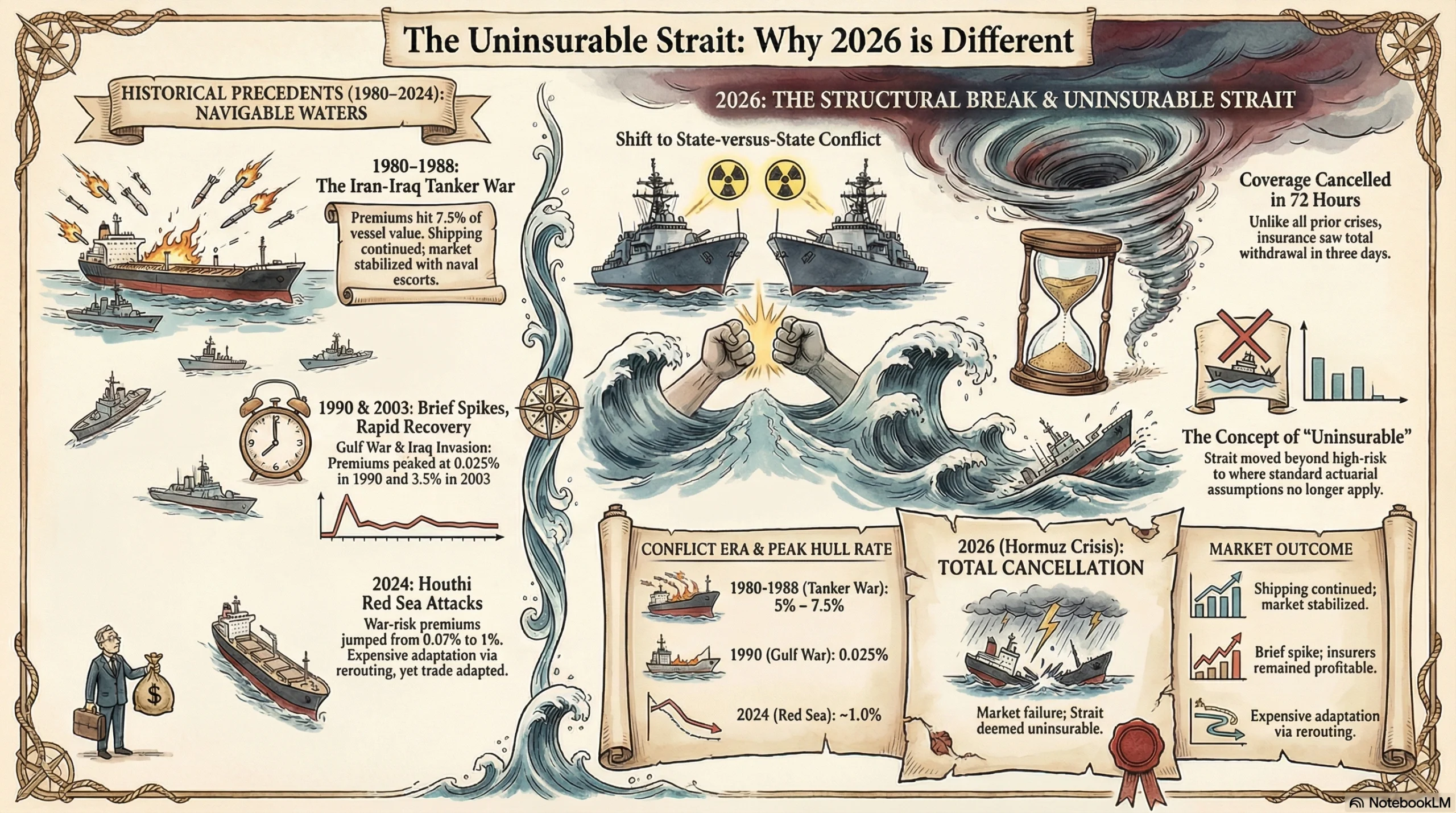

The Hormuz crisis of 2026 is not without precedent. What makes it different — and far more dangerous — is the degree to which it has exceeded every prior historical benchmark.

1980–1988: The Iran-Iraq Tanker War was the most prolonged maritime conflict of the 20th century. Iraq attacked 283 vessels; Iran attacked 168. Cargo premiums surged roughly 300% at the start of hostilities, and hull rates for tankers transiting the Kharg Island terminal reached as high as 5–7.5% of vessel value. Total insurance claims over the eight-year conflict reached approximately $2 billion — a staggering number for the era. And yet, crucially, shipping never stopped. The profit motive outweighed the premium cost. U.S. Navy re-flagging operations and naval escorts, introduced in 1987, eventually stabilized the market and brought rates back down.

1990: The Gulf War was comparatively brief. Premiums rose sharply — to around 0.025% for most Gulf ports, with spikes in the northern Arabian Gulf — but the war ended quickly, merchant shipping suffered minimal damage, and insurers largely came out profitable.

2003: The Iraq Invasion triggered a more acute spike, with hull rates reaching 3.5% around Iraqi waters before falling back to 0.25% within a year as the military situation stabilized.

2024: Houthi Red Sea Attacks — the most recent precedent — saw war-risk premiums for Red Sea transits jump from approximately 0.07% to roughly 1% of hull value. Shipping rerouted around the Cape of Good Hope. Trade adapted, painfully and expensively, but it adapted.

2026 — The difference is structural. In every prior crisis, insurance remained available, and shipping continued at a price. In 2026, insurers cancelled coverage entirely within 72 hours. The strait was not merely dangerous — it was, for practical purposes, uninsurable. Premium rates have blown past all historical precedents within three weeks. And unlike the 1987 scenario, where U.S. naval escorts eventually provided market stability, the current military environment involves direct state-versus-state conflict with a nuclear-threshold adversary. The standard actuarial assumption — that conflicts are localized, temporary, and ultimately survivable for the market — is being tested in real time.

The Strauss Center at UT Austin had long assessed that insurance costs alone would never fully stop Gulf trade. In 2026, that assessment faces its first genuine real-world challenge.

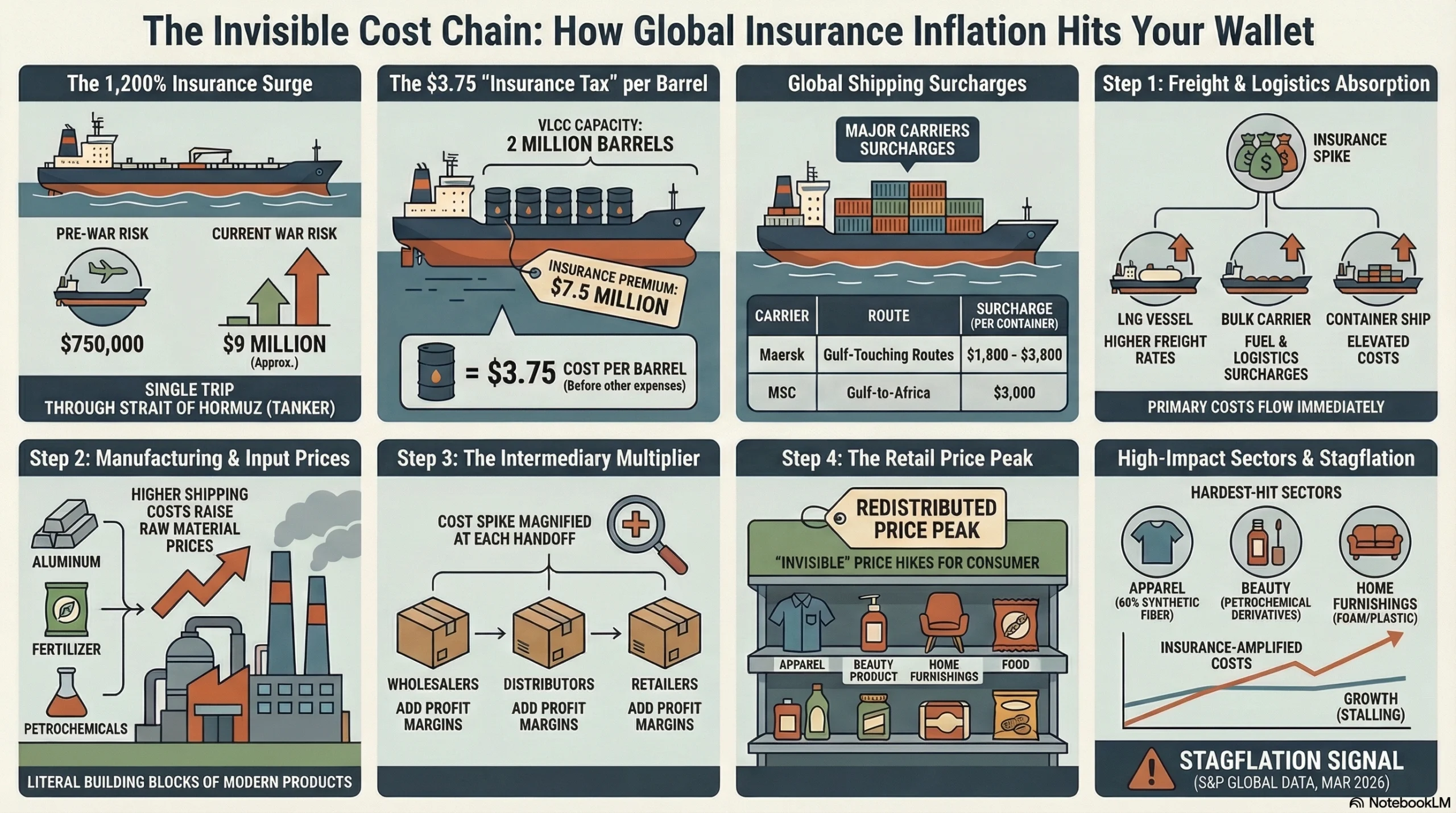

How $7.5 Million in Insurance Becomes $2 More on Your Grocery Bill

The most consequential aspect of the war-risk insurance crisis is the least visible: the way these costs travel through the global supply chain and land, invisibly, in the prices consumers pay for ordinary goods.

Start with the arithmetic. A Very Large Crude Carrier (VLCC) holds approximately 2 million barrels of oil. If war-risk premiums add $7.5 million to a single voyage, that represents roughly $3.75 per barrel added purely from insurance — before the oil price, fuel surcharge, port fees, or any other cost is included. For a $300 million tanker at 3% war-risk rates, a single trip through the Strait of Hormuz now costs approximately $9 million in insurance alone, versus $750,000 before the conflict.

It compounds at every stage. Higher insurance costs flow into higher freight rates. Higher freight rates flow into higher fuel and logistics surcharges. Higher logistics costs flow into higher manufacturing input prices. Higher manufacturing costs flow into higher wholesale prices. Higher wholesale prices flow into higher retail prices — with each intermediary along the chain adding their own margin on top of the elevated cost base. By the time $7.5 million in extra insurance reaches the retail shelf, it has been multiplied and redistributed across an entire product category.

And it’s not just oil tankers. Container ships, LNG carriers, bulk carriers moving aluminum, fertilizer, and chemicals — every vessel class faces the same premium explosion. Maersk added surcharges of $1,800 to $3,800 per container for routes touching the Gulf. MSC added $3,000 per container for Gulf-to-Africa routes. Every container of electronics, apparel, furniture, or food ingredients transiting the region absorbs these costs silently.

As Forbes and Water Tower Research analysis noted in March 2026, “energy is embedded in every cost line — raw materials, manufacturing, transportation and packaging”. Petrochemicals, which are derived from the same oil flowing through Hormuz, are the literal building blocks of product packaging, synthetic fibers, foam cushioning, and plastic components. When oil prices rise and shipping costs rise simultaneously, the feedback loop accelerates.

The sectors hit hardest include:

Home furnishings — foam, aluminum frames, synthetic fabrics, and plastic fittings are all petrochemical-derived and Gulf-logistics-dependent

Apparel — approximately 60% of global apparel uses synthetic fibers (polyester, nylon, spandex), all petroleum-derived

Beauty and personal care — virtually every SKU contains petrochemical derivatives in the formulation or packaging

Food and beverage — packaging, refrigerated transport, and agricultural chemical inputs (fertilizers) are all affected

S&P Global’s flash PMI data for March 2026 shows inflation spiking while growth stalls — the textbook definition of stagflation, and partly the direct result of insurance-amplified cost pass-through moving through every node of the global supply chain. British retailer Next warned in late March that “should these costs endure beyond the next three months, we will start to transfer these costs to consumers through higher prices”.

The key insight for business leaders: unlike tariffs — which are visible, negotiated, and documented — insurance cost increases are invisible to the end buyer. They are embedded in freight quotes, absorbed into supplier invoices, and folded into distributor markups. Most procurement teams don’t even realize they’re paying them. That invisibility is precisely what makes them so dangerous.

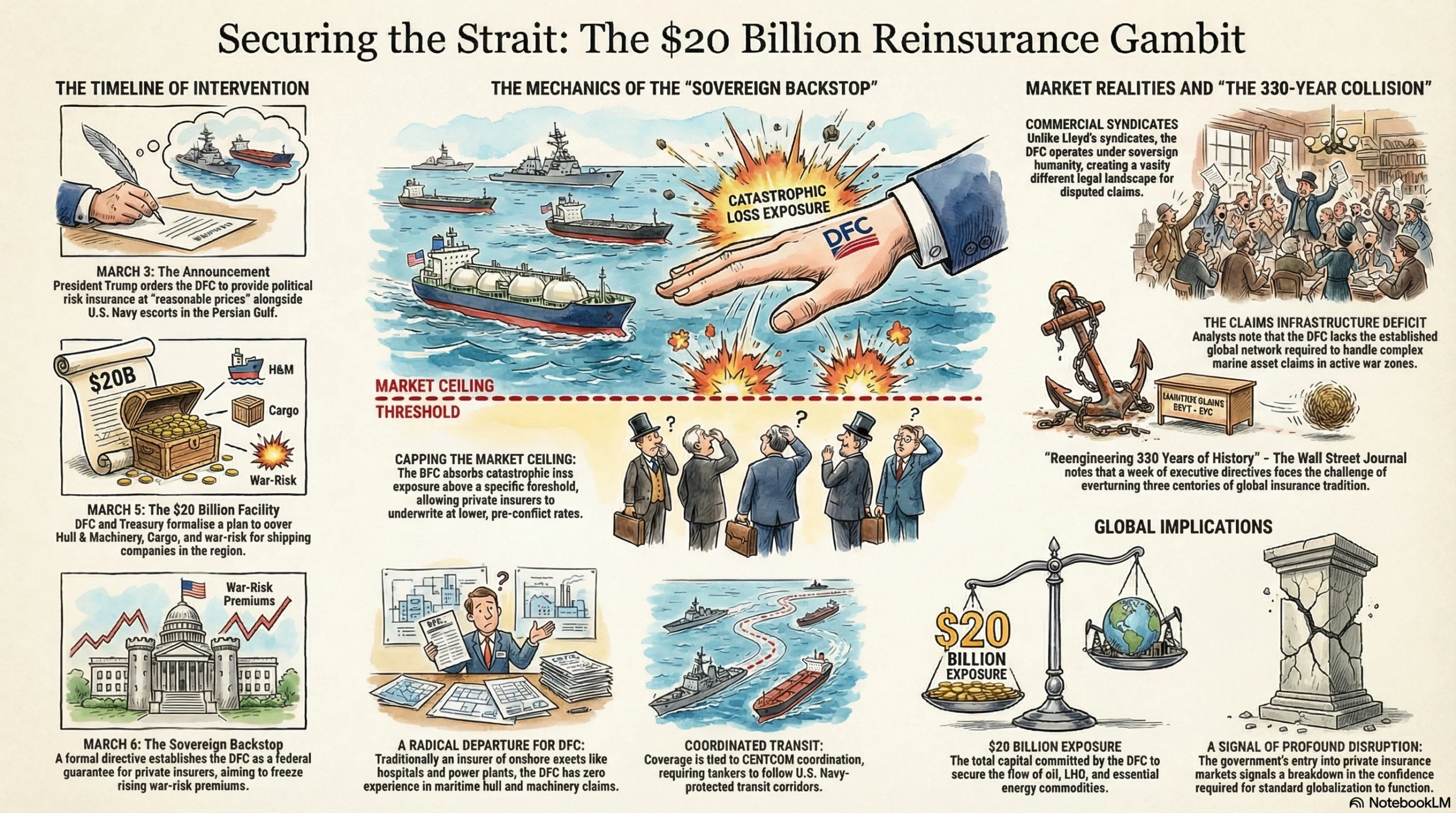

The Government Steps In: A Historic First

On March 3, 2026, President Trump announced on Truth Social that he had ordered the U.S. International Development Finance Corporation (DFC) to extend political risk insurance and guarantees “at a very reasonable price” to secure maritime trade through the Gulf. He also announced that the U.S. Navy would begin escorting tankers through the Strait of Hormuz.

On March 5, DFC CEO Ben Black and Treasury Secretary Scott Bessent formalized the plan: a $20 billion maritime reinsurance facility, covering Hull & Machinery, Cargo, and war-risk coverage for shipping companies operating in the Persian Gulf, in close coordination with CENTCOM.

Why this is historically significant cannot be overstated. The DFC — formerly known as the Overseas Private Investment Corporation (OPIC) — is a U.S. government development finance institution whose normal remit is insuring onshore infrastructure assets in emerging markets: power plants, roads, hospitals. It has zero experience in marine hull and machinery claims. Moving into direct maritime reinsurance for a mobile fleet of hundreds of vessels in an active war zone is, as legal analysts at Clark Hill noted, “a radical departure from the agency’s core competency”.

On March 6, Trump issued a formal directive, effective immediately, ordering the DFC to act as a federal “sovereign backstop” for qualified private insurers providing Hull & Machinery and Cargo coverage in the Persian Gulf. The stated purpose: reduce war-risk premiums and ensure the free flow of oil, LNG, and other energy commodities through the region.

The potential benefit is real. If DFC offers reinsurance capacity near pre-conflict rates, it effectively caps the market ceiling. Private insurers can underwrite at higher rates knowing the government absorbs catastrophic loss exposure above a threshold. The psychological effect on maritime confidence could be as significant as the financial effect.

But serious doubts have emerged. As legal and insurance analysts at MMWR noted, the DFC has no established claims-handling infrastructure for marine assets. Policy wording compatibility with standard Lloyd’s war-risk terms is uncertain. Federal sovereign immunity doctrines apply differently than with commercial syndicates — a ship owner whose claim is disputed by DFC faces a very different legal landscape than one in dispute with a Lloyd’s syndicate. There may be strings attached: mandatory coordination with U.S. Navy transit corridors, specific routing requirements, and compliance obligations that smaller operators may struggle to meet.

The Wall Street Journal reported that the U.S. plan to unblock the strait “collides with realities of global insurance” — realities built over 330 years that cannot be reengineered by executive directive in a week. Lloyd’s CEO acknowledged that coverage “remains available at the right price,” while simultaneously engaging with DFC and meeting with U.S. officials through Marsh, the world’s largest insurance broker.

When the world’s largest economy must step into a private insurance market to keep trade moving, it signals something profound about the scale of the disruption — and about how central insurance confidence is to the functioning of globalization itself.

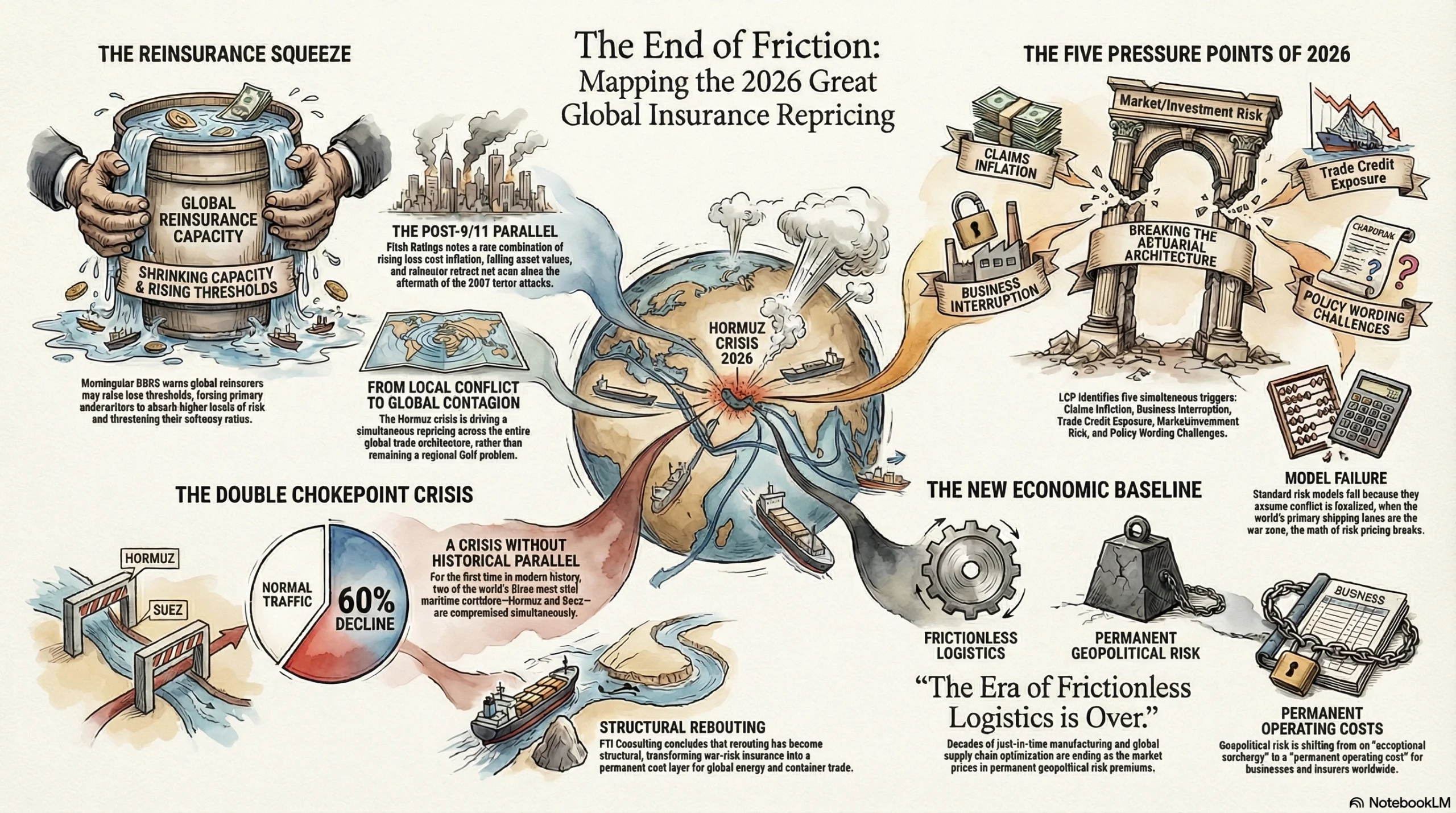

Beyond the Gulf: The Global Repricing of Risk

The 2026 Hormuz crisis is not just a Gulf insurance problem. It is an accelerant that is repricing risk across the entire global insurance and trade architecture simultaneously.

The reinsurance squeeze is tightening. Morningstar DBRS has warned that global reinsurers may raise loss thresholds or reduce capacity in response to extraordinary exposure in the Gulf, leaving primary underwriters absorbing more risk and potentially pressuring their own solvency ratios. Fitch Ratings issued an explicit caution in March 2026 that a prolonged Iran conflict could indirectly affect global insurers through rising loss cost inflation, falling asset values, and reinsurer retreat — a combination not seen since the aftermath of 9/11.

LCP‘s geopolitical risk analysis for 2026 identifies five simultaneous pressure points hitting the insurance sector: claims inflation, business interruption, trade credit exposure, market and investment risk, and policy wording interpretation challenges — all being triggered at once by a single geopolitical event. That is not how insurance risk models are built. Standard actuarial frameworks assume conflict is localized and temporary. When the war zone is the world’s most important shipping lane, the entire mathematical architecture of risk pricing begins to break.

The chokepoint problem is now double. Water Tower Research notes that Red Sea traffic remains down approximately 60% from pre-crisis levels — a disruption that predates the 2026 Hormuz crisis and has never been fully resolved. Two of the world’s three most important maritime chokepoints are now simultaneously compromised: the Red Sea/Suez corridor and the Strait of Hormuz. Together, these two waterways handle an enormous share of global seaborne energy and container trade. Their simultaneous disruption has no historical parallel in the modern global economy.

FTI Consulting‘s analysis of the crisis concluded that “rerouting becomes structural, war-risk insurance becomes a more permanent cost layer, and fuel prices remain elevated as global energy markets adjust”. The operative word is structural — meaning this is not a temporary shock to be absorbed and forgotten. Businesses and insurers alike are beginning to price in a new baseline: a world in which geopolitical risk premiums are a permanent operating cost, not an exceptional surcharge.

The era of frictionless, cheap global logistics — which underpinned decades of globalization, just-in-time manufacturing, and global supply chain optimization — may be structurally over. The market is repricing accordingly.

What Businesses Should Do Now

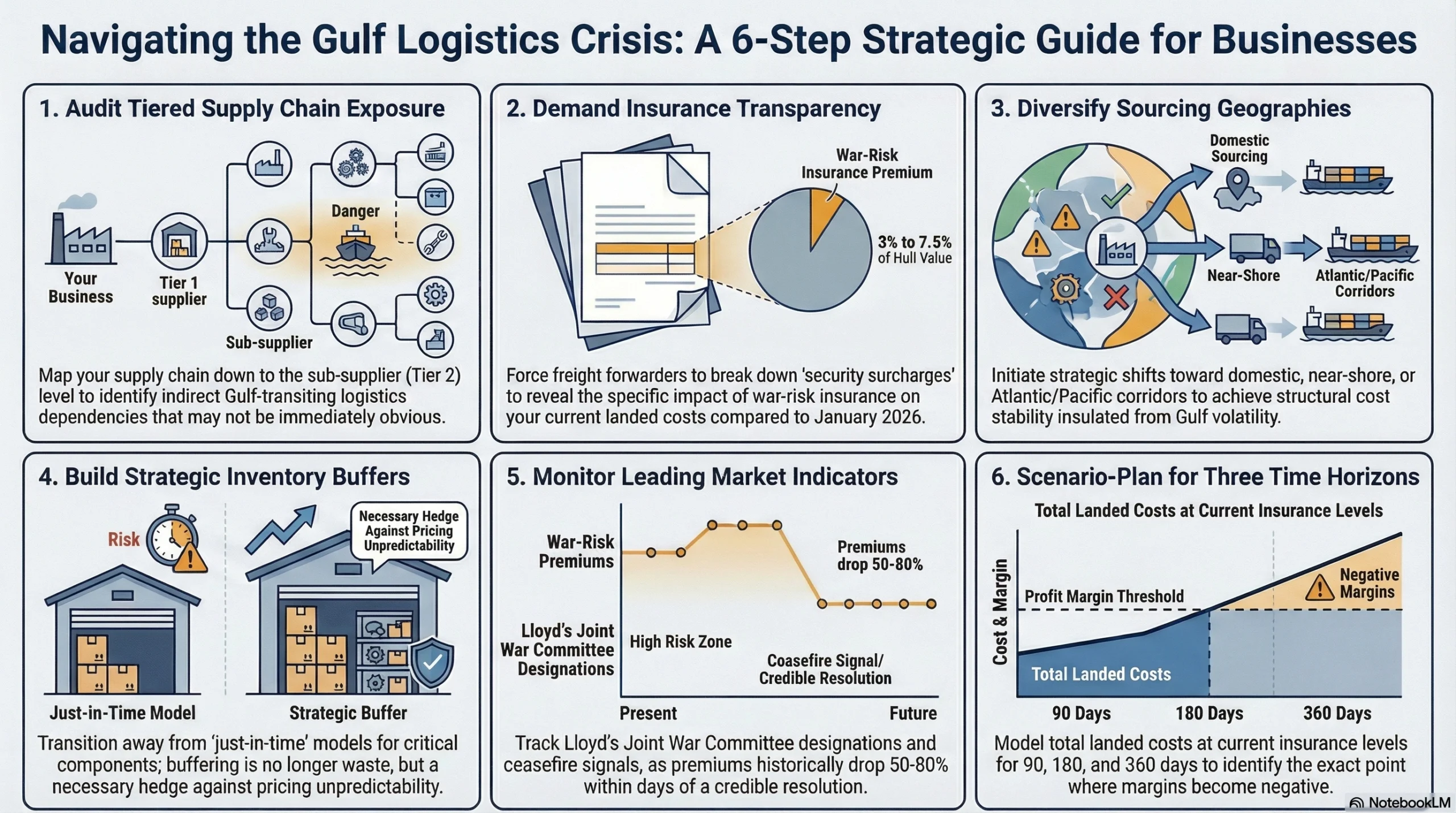

The businesses that navigate this crisis best will be those that act on imperfect information now, rather than waiting for clarity that may take months to arrive. Six actions stand out as immediately actionable.

1. Audit your supply chain for Gulf exposure — including indirect touchpoints.

Your company may not ship directly through Hormuz, but a Tier 2 supplier’s raw materials may. Map your supply chain down to the sub-supplier level and identify which inputs, components, or materials depend on Gulf-transiting logistics. The goal is not to eliminate exposure — that may be impossible — but to quantify it and prepare for it.

2. Demand insurance transparency from your freight forwarders.

War-risk surcharges are routinely buried in line items with vague labels like “security surcharge” or “origin handling fee.” Ask specifically: what portion of my current landed cost is war-risk insurance-driven? What was it in January 2026? Visibility is the prerequisite for control.

3. Diversify sourcing geographies where structurally possible.

Suppliers with production bases insulated from Gulf logistics — domestic, near-shore, or routed through Atlantic and Pacific corridors — offer structural cost stability that current Gulf-dependent suppliers cannot. This is not a short-term fix; it is a medium-term strategic investment. But the sourcing conversations should begin now.

4. Build inventory buffers for critical inputs.

The just-in-time model assumes stable, predictable logistics. That assumption is broken. For components or materials with long lead times or single-source dependencies in the Gulf region, deliberate inventory buffering is not waste — it is risk management. Euronews analyst Camillo Forgione noted that businesses face not just cost pressure but unpredictability — the inability to quote accurate prices forward.

5. Monitor for ceasefire signals and corridor developments.

History shows that war-risk premiums drop rapidly — 50% to 80% within days — once credible ceasefire agreements are reached or sustained naval escorts become operational. The DFC reinsurance facility, if it becomes operational and credible, could trigger a similar market correction. Businesses that have flexibility in their procurement timing should position for that buying window. Watch Lloyd’s Joint War Committee designations closely — they are the leading indicator.

6. Scenario-plan for duration across three time horizons.

Model your total landed cost on Gulf-sourced goods at current insurance levels (3–7.5% of hull value) for 90 days, 180 days, and 12 months. Identify at which point each scenario triggers a break-even or margin-negative position. That analysis will tell you which sourcing or pricing decisions cannot wait, and which can be deferred pending market resolution.

Oliver Wyman’s supply chain analysis for March 2026 emphasizes that the businesses best positioned to survive prolonged disruption are those that have invested in visibility, flexibility, and optionality — not just cost optimization. The crisis is stress-testing a decade of supply chain decisions made under the assumption that globalization was an unconditional structural advantage.

Conclusion: The Price of Uncertainty

War-risk insurance is the canary in the coal mine of globalization. When the cost of insuring trade becomes more disruptive than the cost of the goods themselves, something fundamental has shifted.

The 2026 Hormuz crisis has revealed, in quantitative terms, exactly how the global economy is wired — and where its most critical single points of failure lie. A 330-year-old market, built on handshakes in a London coffee house, now has the power to halt the flow of 20% of the world’s oil with a 72-hour cancellation notice. And when that market fails, no amount of executive directive can instantly replace the confidence that has evaporated.

The premium surge documented here — from 0.25% to 7.5%, from $250,000 to $7.5 million per voyage, in under three weeks — is not just a data point. It is a price signal. Markets are telling us that the infrastructure of confidence underpinning global trade has been severely damaged, and that rebuilding it will take more than a government reinsurance facility, however well-capitalized.

Every business that sources globally, ships globally, or prices goods in a market touched by global logistics is now paying the invisible tax. The question is no longer whether you’re exposed. The question is whether you know how much — and what you’re going to do about it.

FAQs

War-risk insurance is a specialized marine policy covering losses caused by war, terrorism, piracy, mines, hostile acts, and government seizure. It is explicitly excluded from all standard marine insurance policies and must be purchased separately. Without it, ships cannot dock, cargo cannot be loaded, and voyages cannot be financed.

Premiums surged from approximately 0.25% of vessel hull value before the conflict to 3.5–7.5% by week three — with some high-risk vessels facing quotes at 10% or more. That represents premium increases of 1,000% or more in under three weeks.

At least seven major P&I Clubs issued 72-hour cancellation notices after Iran’s IRGC declared the Strait of Hormuz “closed” and multiple vessels were attacked. Standard war-risk policy wording allows for rapid cancellation in response to declared conflict or imminent physical threat.

War-risk costs are embedded in freight rates, supplier invoices, and distributor markups, invisibly raising the landed cost of goods from oil to groceries to electronics. Because they are not line-itemized in most consumer-facing pricing, they are effectively an invisible tax on global trade.

Yes. President Trump ordered the DFC to act as a federal “sovereign backstop” reinsurer for Gulf maritime shipping on March 6, 2026, committing up to $20 billion in reinsurance capacity. This is historically unprecedented for an agency with no prior marine claims experience.

The 1980s Tanker War saw hull rates of approximately 5% over eight years, with $2 billion in claims. In 2026, those premium levels were reached within two weeks — and insurers began cancelling coverage entirely, a step never taken in prior Gulf conflicts.

Historically, war-risk premiums drop sharply — often 50–80% — within days of a credible ceasefire or the establishment of reliable naval escort corridors. However, structural repricing of geopolitical risk is likely to keep baseline rates elevated above pre-2024 levels for years, even after the immediate crisis resolves.

Audit your supply chain for Gulf touchpoints, demand transparency from freight forwarders on insurance line items, diversify sourcing geographies, build inventory buffers for critical inputs, monitor ceasefire signals as buying windows, and scenario-plan your cost model at current premium levels across 3-, 6-, and 12-month horizons.