When China chose December 18—the anniversary associated with the start of Reform and Opening-up—to activate island-wide “special customs operations” for the Hainan Free Trade Port, the symbolism was unmistakable. But the strategic implications extend far beyond tariff reductions, duty-free shopping narratives, or port modernization. In the official framing, the Hainan FTP now operates under a special customs supervision system characterized by “freer access at the first line” (between Hainan and overseas) and “regulated access at the second line” (between Hainan and the mainland), enabling freer flows of goods, capital, personnel, and data under a simplified and expanded “zero-tariff” regime. Source

For decision-makers in supply chain, finance, and geopolitical risk, Hainan is increasingly interpreted less as a conventional “free port” and more as a physical and institutional platform for what Chinese strategic discussions sometimes call a “second division of labor system” (第二个分工体系): a China-centered economic architecture that can operate parallel to, and under stress potentially partially independent from, the post–WWII system dominated by the dollar, SWIFT-centered messaging, and Western legal-institutional defaults. A critical reason this framing resonates is that today’s “default” order is not merely political—it is infrastructural. The U.S. Federal Reserve’s synthesis of dollar dominance emphasizes how the dollar’s role is supported by deep and liquid markets, safe-asset demand, and institutional trust—qualities that compound over time into powerful network effects. Source

This analysis explores five core questions:

What is this “second division of labor system,” and how does it differ from the existing global order?

How does Hainan fit into China’s RMB internationalization and multi-CBDC settlement strategy (notably mBridge)?

What is China’s “Malacca dilemma,” and how could Hainan contribute to risk diversification?

How is China–ASEAN industrial organization evolving, and how might Hainan become an anchor node?

Are we moving toward global trade fragmentation or a more interoperable multipolar system?

The stage-setting data points are not just abstract geopolitical talking points. Hainan’s policies explicitly increase the share of “zero-tariff” products and introduce a crucial industrial lever: zero-tariff goods processed in Hainan may be sold to the mainland duty-free if local processing adds at least 30% value—a rule designed to reshape value capture and manufacturing geography, not merely reduce costs. Source

Meanwhile, the People’s Bank of China has explicitly framed financial preparation as integral, highlighting Hainan’s EF accounts and reporting that by end-October 2025, 11 banks in Hainan opened 658 EF accounts with 268.9 billion yuan in transactions across 80 countries/regions. Source

The "Second Division of Labor System"—Conceptual Framework

Understanding the "First System"—The Post-WWII Architecture

The “first system” is not one treaty or one institution; it is an ecosystem. Its durability comes from stacked network effects—currency, payments, legal norms, and geography reinforcing each other. The point is not that it is “Western” in a cultural sense; the point is that many firms treat it as the default operating environment because it minimizes friction.

1) Dollar-denominated trade and monetary gravity.

The U.S. dollar’s dominance persists because it combines liquidity, deep markets, and trust-based demand for safe assets. The U.S. Federal Reserve’s 2025 review notes the dollar comprised 58% of disclosed global official foreign reserves in 2024 and argues that the dollar’s role remains stable across multiple dimensions of international usage. Source

2) Western-aligned institutions and the “rules layer.”

Even when firms operate far from U.S. and European borders, contracts, compliance expectations, and dispute-resolution preferences often inherit “default settings” that reflect the incumbent system’s legal predictability. What matters for executives is not ideology but enforcement: lower enforcement risk reduces capital costs and widens the feasible set of counterparties. This institutional trust interacts with the currency layer: reserve currency status strengthens a jurisdiction’s financial influence, and predictable institutions strengthen reserve currency status. The persistence of these feedback loops is a central theme in the Fed’s baseline assessment of why dollar dominance remains durable absent “large-scale, lasting disruptions.” Source

3) Messaging and correspondent banking rails.

The “first system” is also technical. Cross-border payment routing—especially for trade and treasury operations—often flows through established correspondent networks whose operational standards are widely embedded across banks. Even when currency diversification occurs, the messaging and compliance stack can remain anchored to incumbent pathways. The Fed note explicitly uses SWIFT international payments as a key indicator of transaction dominance and persistence. Source

4) Hub geography and chokepoint economics.

The “first system” naturally concentrates around hubs because concentration reduces coordination costs: more counterparties, more liquidity, more specialized services (trade finance, insurance, arbitration, compliance). While this blog will later discuss maritime chokepoints, the deeper point is institutional: hubs are where logistics and finance fuse into a single service ecosystem, and ecosystems tend to exhibit winner-take-most dynamics.

5) Technology and standards.

Standards become governance. Once compliance expectations, message formats, and operational norms are embedded, they are difficult to displace without a meaningful economic payoff. This is why the “first system” persists even as geopolitics shifts: cost-saving alternatives must be large enough to overcome switching frictions.

The "Second System" China is Building

China’s “second system” is best understood as parallel infrastructure that can reroute trade, settlement, and industrial organization without requiring immediate, full replacement of the incumbent order.

1) Alternative payment infrastructure: mBridge as a multi-CBDC corridor.

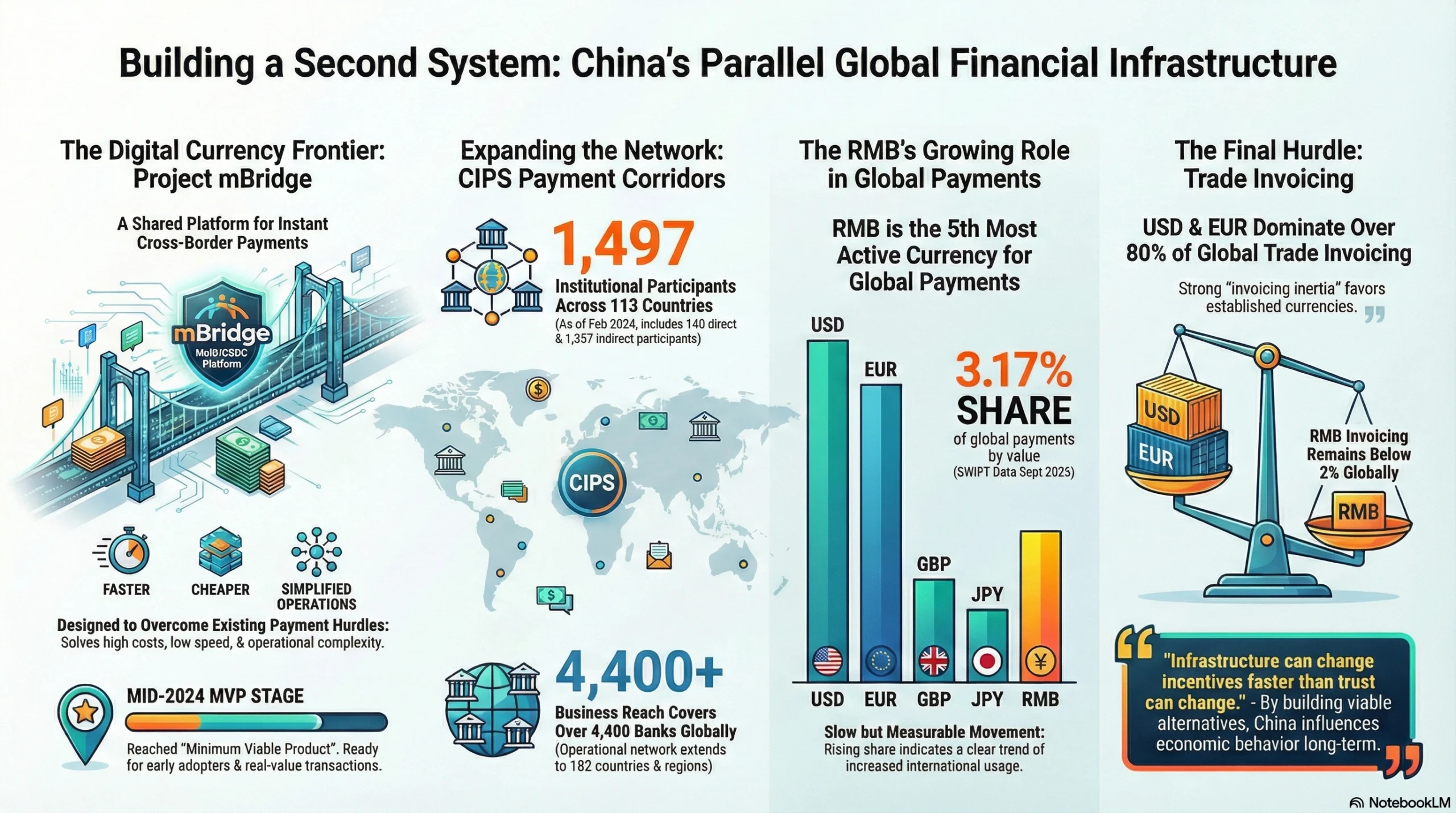

The BIS confirms Project mBridge reached MVP stage in mid-2024 and is designed to enable instant cross-border payments and settlement on a shared multi-CBDC platform built on distributed ledger technology (DLT). Source

The BIS press release frames mBridge’s intent: addressing high cost, low speed, and operational complexities in cross-border payments, with a governance and legal framework (including a rulebook) tailored to a decentralized architecture. Source

HKMA’s announcement reinforces that mBridge’s MVP is meant for early adopters conducting real-value transactions with validating nodes deployed in each jurisdiction. Source

2) RMB payment corridors: CIPS as scaling infrastructure.

CIPS participation is a key indicator of institutional reach. As of February 2024, CIPS had 1,497 participants (140 direct, 1,357 indirect) across 113 countries/regions, and its business covers more than 4,400 banking institutions in 182 countries/regions. Source

3) The slow but real shift in RMB usage.

SWIFT’s RMB Tracker shows that in September 2025 the RMB was the 5th most active currency for global payments, with a 3.17% share by value (and 2.34% excluding Eurozone payments). That is not dominance, but it is measurable movement. Source

4) Invoicing inertia remains strong.

ECB analysis finds the USD and EUR together account for over 80% of global trade invoicing, while RMB invoicing remains below 2% globally (though rising in some regions). This is the core reason infrastructure matters: it can change incentives faster than trust can change. Source

Key Distinctions—Not a Complete Bifurcation

This is not a full decoupling story. It is about building redundant pathways so that China-linked trade can keep functioning under pressure. The Fed’s view underscores that dollar dominance is resilient and tied to market depth and institutional trust. Source

Meanwhile, the ECB emphasizes invoicing patterns remain broadly stable even amid geopolitical tensions and that “lock-in effects and network externalities” help explain persistence. Source

So the operational expectation for businesses should be coexistence: multiple systems that overlap, with corridor-specific adoption based on cost, compliance, and geopolitical risk.

Hainan's Role in This Architecture

Hainan matters because it connects the “rules layer,” “logistics layer,” and “finance layer” into a single experimental platform.

1) Testing ground for new rules (trade + industrial policy).

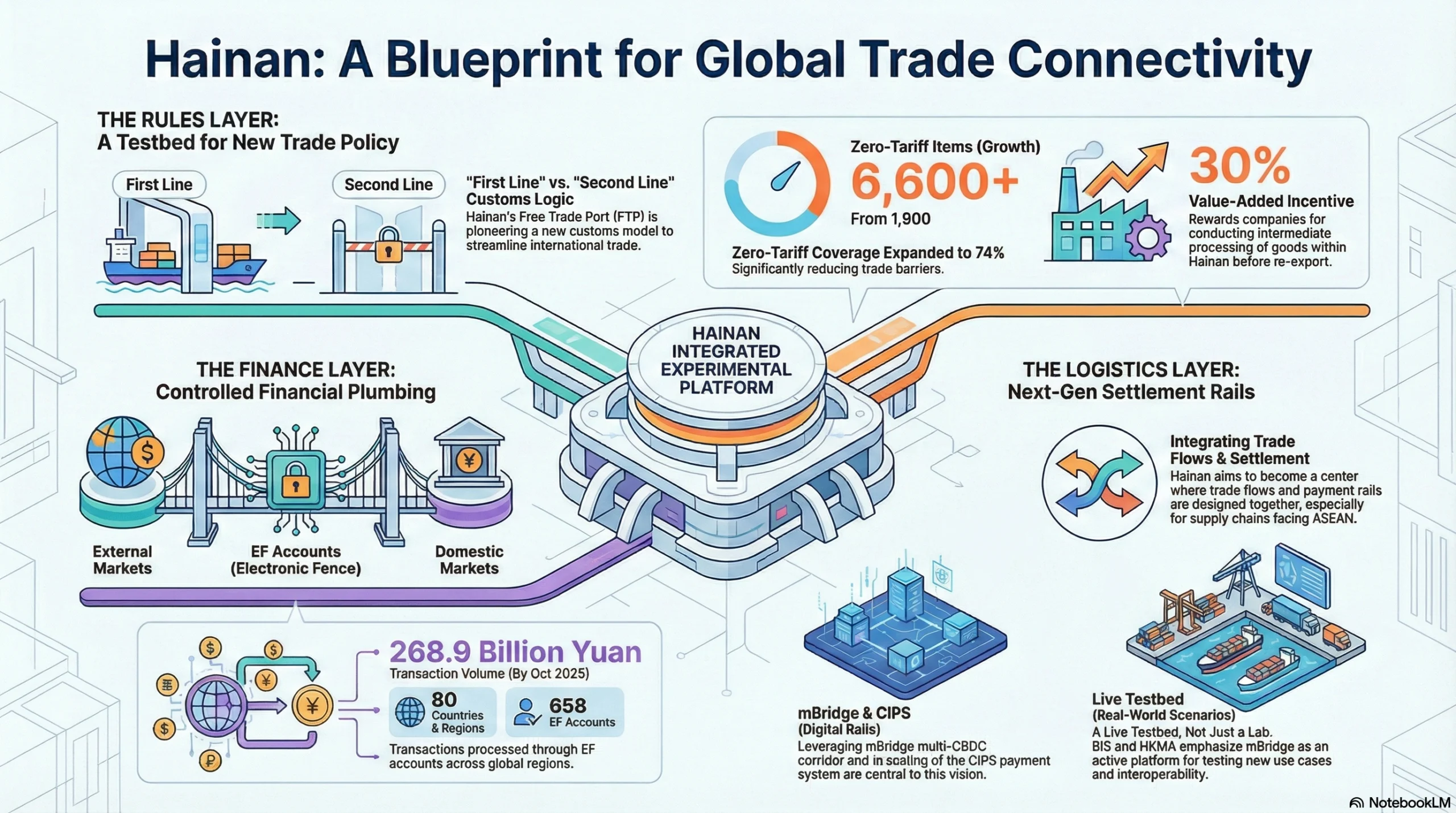

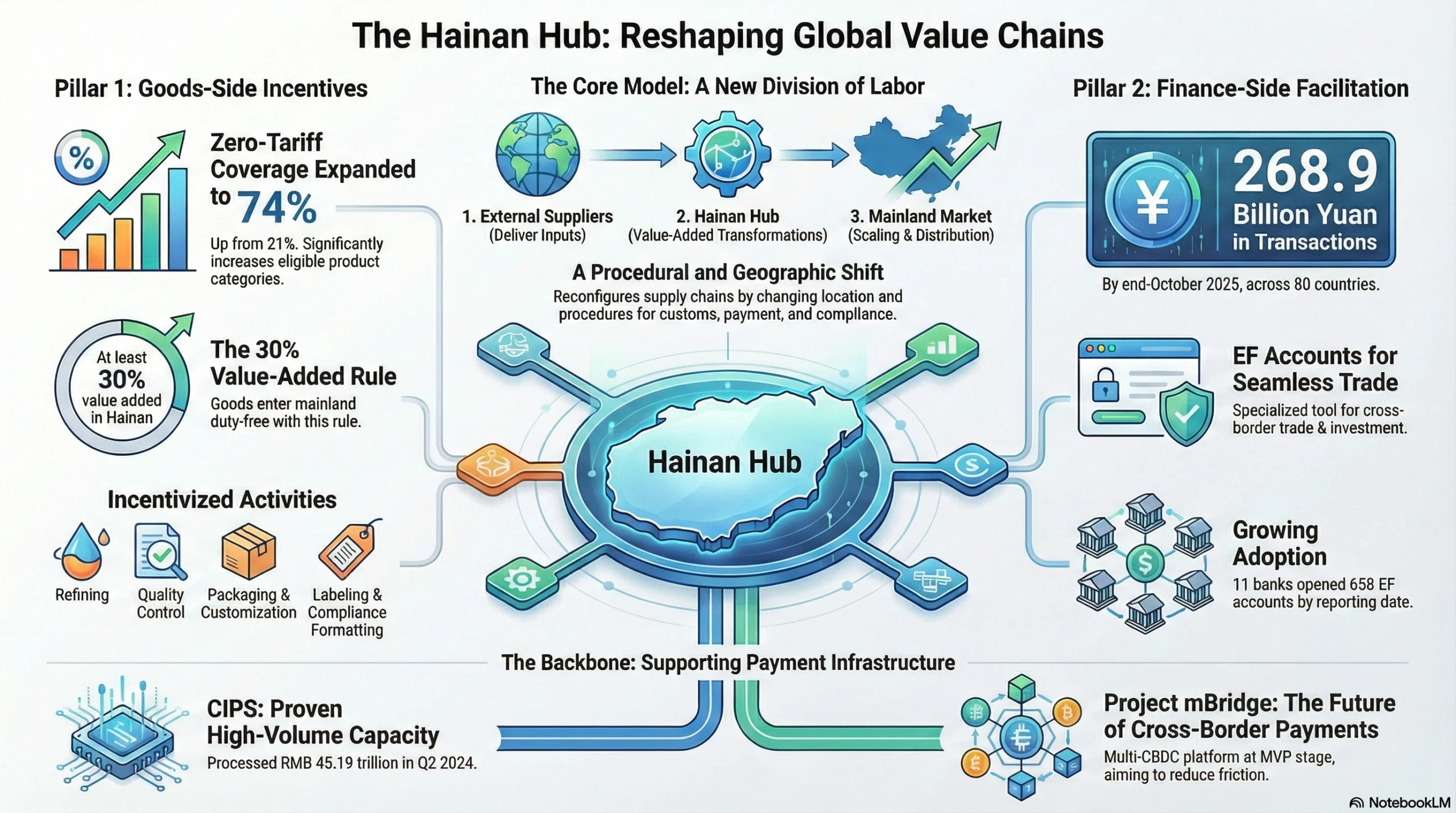

The Hainan FTP’s model introduces “first line” vs “second line” customs logic, expands zero-tariff coverage from 21 to 74 percent (from 1,900 to over 6,600 items), and operationalizes the 30% value-added pathway that rewards intermediate processing in Hainan. Source

2) Financial plumbing: EF accounts as controlled openness.

PBOC’s reported rollout of EF accounts is part of building a controlled interface between external and domestic markets; it discloses 658 EF accounts and 268.9 billion yuan in transactions across 80 countries/regions by end-October 2025. Source

3) Settlement and payment rails nearby.

If mBridge’s multi-CBDC corridor matures and CIPS continues scaling, Hainan can become a place where trade flows and settlement rails are designed together—particularly for ASEAN-facing supply chains. This premise aligns with the BIS/HKMA emphasis that the mBridge MVP is a testbed for new use cases and interoperability, not merely a laboratory prototype. Source

Financial Infrastructure—RMB Internationalization and mBridge

The Challenge of RMB Internationalization

RMB internationalization faces a fundamental contradiction: China is a dominant trade and manufacturing power, but its currency’s global usage remains far below the dollar’s. The Fed explicitly notes structural constraints—limited convertibility, a not-fully-open capital account, and investor confidence issues—that reduce the RMB’s attractiveness as a reserve currency and broad medium of exchange. Source

From the invoicing perspective, the ECB’s dataset-driven analysis underscores how sticky currency equilibria are: the USD and EUR remain the primary invoicing currencies (over 80% combined), and RMB invoicing remains low globally. That doesn’t mean RMB is irrelevant; it means its growth is likely to be corridor-specific and policy-assisted rather than spontaneous and universal. Source

From the payments perspective, SWIFT’s RMB Tracker offers a clear reality check: RMB at 3.17% of global payments by value in September 2025—growing, but still a minority share in the global system. Source

For global firms, the strategic question is not “will RMB replace USD?” but: where can RMB-based settlement be cheaper/faster, and how can treasury operations remain robust under geopolitical stress? The logic of a “second division of labor system” is thus less about replacing the first system and more about widening the feasible operating set under risk—especially for trade corridors where China is the dominant end-market, where switching costs can be justified by policy-induced incentives, and where participants are willing to co-evolve compliance processes alongside new rails.

mBridge—The CBDC Alternative Pathway

mBridge is a settlement infrastructure bet. In the BIS framing, it is a multi-central bank digital currency platform intended to deliver instant cross-border payments and settlement, built on DLT, and designed to reduce the cost and complexity associated with correspondent banking. Source

The BIS press release adds operational detail: mBridge includes a bespoke governance and legal framework (rulebook), validating nodes in each jurisdiction, and compatibility with the Ethereum Virtual Machine—explicitly positioning it as a testbed for add-ons and interoperability. Source

HKMA’s press release highlights the MVP logic: it is “a basic version” intended for early adopters and iterative enhancement before full production, and the platform is meant to widen participation over time. Source

In practical terms, mBridge is an attempt to shift the adoption curve by making settlement efficiency gains large enough to justify behavioral change—even when “trust” and “market depth” aren’t yet at dollar-system levels. In the language of policy design, mBridge is not just a payments innovation: it is an institutional experiment in governance across jurisdictions where “who validates,” “who sets rules,” and “how compliance is encoded” becomes part of the platform itself, not an external overlay.

Hainan's Financial Role—The Missing Piece

Hainan’s distinctive contribution is not that it “creates” the RMB’s global role, but that it provides a high-policy-flexibility location where financial tools and trade incentives can be combined.

PBOC’s preparation work, as reported by Xinhua, emphasizes EF accounts for cross-border capital flow convenience and reports: 658 EF accounts, 268.9B yuan in transactions across 80 countries/regions by end-Oct 2025. This indicates deliberate capacity-building rather than a symbolic pilot. Source

On the system-level payments side, PBOC’s Payment System Report (Q2 2024) shows that CIPS processed 2.1292 million transactions totaling RMB45.19 trillion in Q2 2024 (with daily averages of 31,300 transactions and RMB664.555 billion), highlighting that China’s cross-border RMB plumbing is operating at large scale. Source

And the CIPS operator’s own disclosure shows that participation reached 1,497 by February 2024, spanning 113 countries/regions—key for network viability. Source

Combine this with Hainan’s customs incentives (expanded zero-tariff list + 30% value-added pathway), and the logic emerges: Hainan is built to be a place where trade activity generates natural demand for cross-border settlement tools, rather than expecting firms to adopt new financial rails without clear commercial use cases. Source

Realistic Assessment—Will This Work?

Three realities set the boundary conditions:

The dollar system remains entrenched. The Fed emphasizes the depth and liquidity of U.S. financial markets and the dollar’s continued dominance in reserves and transactions. Source

Invoicing patterns change slowly. The ECB’s global invoicing data show stability and lock-in effects, even amid geopolitical shock. Source

Payments and corridors can shift faster than invoicing. SWIFT’s RMB Tracker demonstrates incremental but real changes in payment share. Source

The likely outcome is not global RMB dominance, but meaningful corridor-specific expansion—especially where Hainan provides the trade, processing, and tariff incentives that make RMB settlement economically attractive. For executives, this should translate into a practical question set: where do customers demand RMB pricing; where can suppliers accept it without balance-sheet strain; what banking partners can clear reliably; and what internal controls and documentation changes would be required to operate in a dual-rail environment.

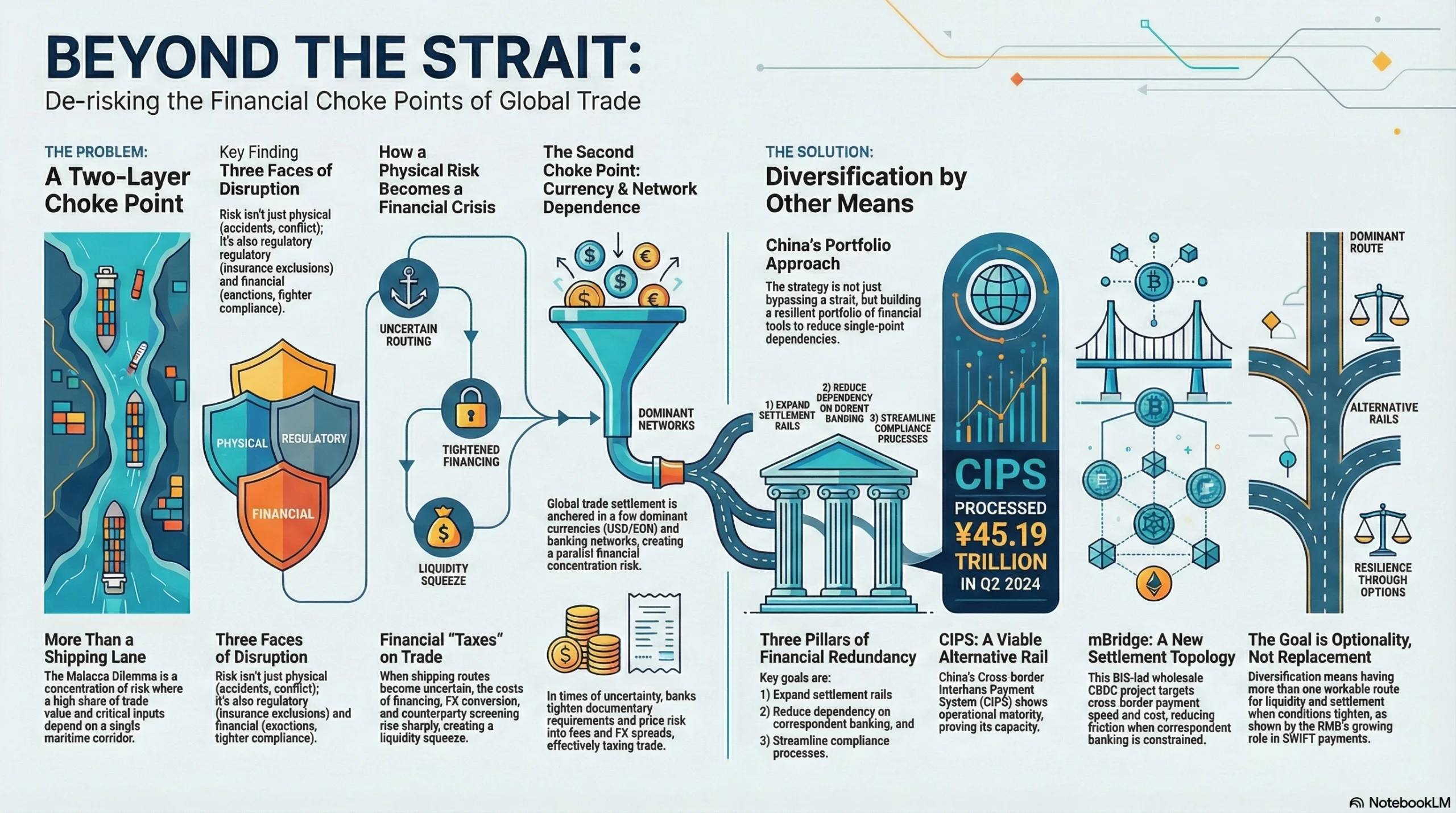

The Malacca Dilemma—Geographic Diversification Strategy

The “Malacca Dilemma” is often introduced as geography—a narrow maritime corridor that sits on the shortest sea-lane connecting the Indian Ocean energy and raw-material exporters with East Asian manufacturing and consumer markets. But for firms and policymakers, the deeper problem is risk concentration: when a high share of trade value, critical inputs, and working-capital cycles depend on a single corridor, disruption becomes a balance-sheet event. That disruption may be physical (accident, congestion, conflict), regulatory (insurance exclusions, port access constraints), or financial (sanctions, de-risking, tighter compliance). In practice, the choke point is not only a shipping problem; it is a settlement and documentation problem—because the moment routing becomes uncertain, the costs of financing, FX conversion, and counterparty screening rise sharply, precisely when firms most need predictable liquidity. This is the terrain where financial infrastructure can act as a form of “geographic diversification by other means.” ECB

From an international monetary perspective, the Malacca dilemma interacts with a second concentration problem: global trade settlement is structurally anchored in a small set of dominant currencies and networks. The European Central Bank’s annual review of the international role of the euro underscores how global invoicing, funding markets, and payment infrastructures remain highly centralized even as trade becomes more regionally fragmented. In other words, even if cargo is rerouted, many firms remain dependent on dollar/euro liquidity, correspondent banking relationships, and compliance gatekeepers. That dependence can translate a physical chokepoint into a financial chokepoint: when routing uncertainty increases, banks tighten documentary requirements, add buffers to timelines, and price risk into fees and FX spreads—effectively taxing trade. ECB

This is why China’s “diversification” play should be read less as a single project to bypass a strait and more as a portfolio approach: (1) expand redundancy in settlement rails; (2) reduce single-point dependency on correspondent banking; and (3) bundle trade, customs, and finance into repeatable compliance processes. Here, the strategic logic links to the build-out of RMB cross-border settlement, messaging/clearing alternatives, and programmable settlement experiments—tools that can reduce settlement friction even when physical logistics become volatile.

At the infrastructure level, the People’s Bank of China’s payment system reporting provides a baseline for the scale and operational maturity of China’s cross-border plumbing. CIPS activity is not just a policy slogan: it is measurable throughput. The PBOC’s Payment System Report (Q2 2024) reports that the Cross-border Interbank Payment System processed 2.1292 million transactions totaling RMB45.19 trillion, which signals an ability to clear and settle large cross-border values even as global finance becomes more compliance-intensive. PBOC

In parallel, BIS-led wholesale CBDC experimentation reframes diversification again: not “new money,” but new settlement topology. Project mBridge—developed with the BIS Innovation Hub and partner central banks—targets pain points in cross-border payments: speed, cost, and operational complexity. The relevance to the Malacca dilemma is indirect but critical: when physical routing risk rises, firms need settlement certainty, faster liquidity turnover, and lower operational friction (especially where correspondent relationships are constrained or expensive). BIS materials emphasize that mBridge’s design is multi-jurisdictional with governance and legal considerations built in—precisely the kind of infrastructure that aims to reduce “single-gate” vulnerabilities in the financial layer. BIS

Finally, SWIFT’s RMB Tracker illustrates how the settlement layer is already pluralizing: RMB’s role in global payments remains modest relative to USD/EUR, but it is observable, measurable, and operational—meaning that in certain corridors, firms can diversify currency and settlement choices even while maintaining parallel use of incumbent rails. For the Malacca dilemma framing, this matters because diversification is rarely binary; it is incremental optionality—having more than one workable route for liquidity, documentation, and settlement timing when conditions tighten. SWIFT

Understanding China's Strategic Vulnerability

China’s strategic vulnerability begins with geography, but it is amplified by institutional and financial realities: trade corridors are “tight-coupled systems,” where shipping schedules, customs clearance, documentary compliance, and payments form one continuous pipeline. When the pipeline is stressed, the failure mode is often not a ship stopping; it is a cash conversion cycle breaking—letters of credit delayed, documents rejected, FX hedges mismatched, or treasury teams forced to pay higher spreads for same-day liquidity.

This is the “second-order” Malacca dilemma: even if alternative maritime routes exist, the financial and compliance layer can still bottleneck trade if settlement is slow, costly, or dependent on a narrow set of correspondent relationships. That is why China’s mitigation strategy increasingly emphasizes payment and settlement infrastructures that can operate at scale, shorten settlement time, and reduce points of discretionary friction.

1) RMB cross-border plumbing at scale (CIPS as capacity, not rhetoric). The operational relevance of CIPS is that it offers a clearing/settlement backbone that can support RMB-denominated trade and finance at meaningful volume. The PBOC’s Q2 2024 report—showing 2.1292 million CIPS transactions totaling RMB45.19 trillion—is best read as “capacity under real conditions,” not as a future ambition. For firms, capacity matters because it affects whether diversification is practical: it determines processing resilience, cut-off times, and the ability to scale corridor-specific RMB settlement when disruptions increase compliance friction on other rails. PBOC

2) mBridge and the settlement-speed objective (liquidity turnover under stress). BIS and the Hong Kong Monetary Authority position mBridge as an effort to improve cross-border payment speed and efficiency using distributed ledger technology with multi-central bank participation. The strategic relevance is not “replacing SWIFT,” but reducing the time and operational risk embedded in cross-border settlement—especially for corridor trade where liquidity turnover becomes critical during disruption. Faster settlement can reduce the amount of working capital trapped “in transit,” which is exactly what spikes when logistics become uncertain. BIS HKMA

3) Hainan EF accounts as an institutional interface (reduce capital-flow friction). The PBOC’s disclosures on Hainan’s financial preparation for island-wide special customs operations highlight EF accounts as a mechanism to integrate local and foreign currency flows in a controlled, policy-designed environment. In the Malacca-dilemma frame, this is a “collection hub” logic: if uncertainty rises in the external environment, firms benefit from a predictable interface where documentation, settlement choices, and compliance can be standardized before goods (and payments) enter the mainland market. PBOC/Xinhua

Across these layers, the key idea is not to claim that geography stops mattering; it is that vulnerability can be priced down through institutional design. Over time, the more that settlement rails (CIPS), multi-party innovation (mBridge), and policy interfaces (EF accounts within Hainan’s broader trade regime) become routinized, the more China can treat chokepoint exposure as a managed operational risk rather than an existential dependency—while global firms operating in Asia gain a broader menu of treasury and settlement options in an increasingly fragmented world. CIPS SWIFT ECB

China-ASEAN Industrial Chain Reconfiguration

The Evolving Division of Labor

The key shift in the emerging “Hainan hub” model is that value capture is being pulled into China-administered policy zones, rather than remaining only at offshore trade hubs or purely within the mainland.

Hainan’s island-wide special customs operations materially change the location of intermediate value creation. The policy expands zero-tariff coverage from 21% to 74% of products, and also embeds a rule that processed goods can enter the mainland duty-free if value-added reaches 30%—which explicitly incentivizes intermediate steps (refining, quality control, packaging, customization, labeling, testing documentation, and compliance formatting) to occur inside Hainan before “second line” entry into the mainland market. Source

This goods-side incentive is paired with a finance-side operating layer. The People’s Bank of China describes EF accounts as part of the financial preparation for Hainan’s island-wide special customs operations, designed to facilitate cross-border trade and investment flows under the FTP regime. Adoption metrics matter because they indicate whether the system is becoming operational rather than aspirational: by end-October 2025, 11 banks in Hainan had opened 658 EF accounts, and these accounts had handled 268.9 billion yuan in transactions across 80 countries/regions. Source

Taken together, Hainan is not merely a “trade” node; it is an attempt to reshape industrial organization through a repeatable interface: external suppliers deliver inputs, Hainan performs intermediate value-added transformations under an incentivized rule set, and the mainland absorbs higher-value manufacturing, scaling, and distribution. The “reconfiguration” is therefore not only geographic—it is procedural. When customs policy (zero-tariff coverage and the 30% value-added threshold) is combined with trade-finance facilitation (EF accounts), the zone can standardize documentation, payment timing, and compliance steps—reducing friction for firms that run multi-country supply chains.

That model becomes more credible when placed beside China’s existing settlement infrastructure. The PBOC’s Payment System Report (Q2 2024) shows that CIPS processed 2.1292 million transactions totaling RMB45.19 trillion in that quarter—evidence of large-scale cross-border settlement capacity that can support real trade flows once a corridor standardizes its documentation and counterparties. Meanwhile, Project mBridge is explicitly framed by the BIS (and echoed by HKMA) as a multi-CBDC platform that has reached Minimum Viable Product (MVP) stage and is designed to broaden participation, operate with a governance and legal framework, and support real-value transaction experimentation—i.e., an infrastructure layer intended to reduce cross-border payment friction where traditional rails are costly or slow. Source Source Source

Industry-Specific Examples

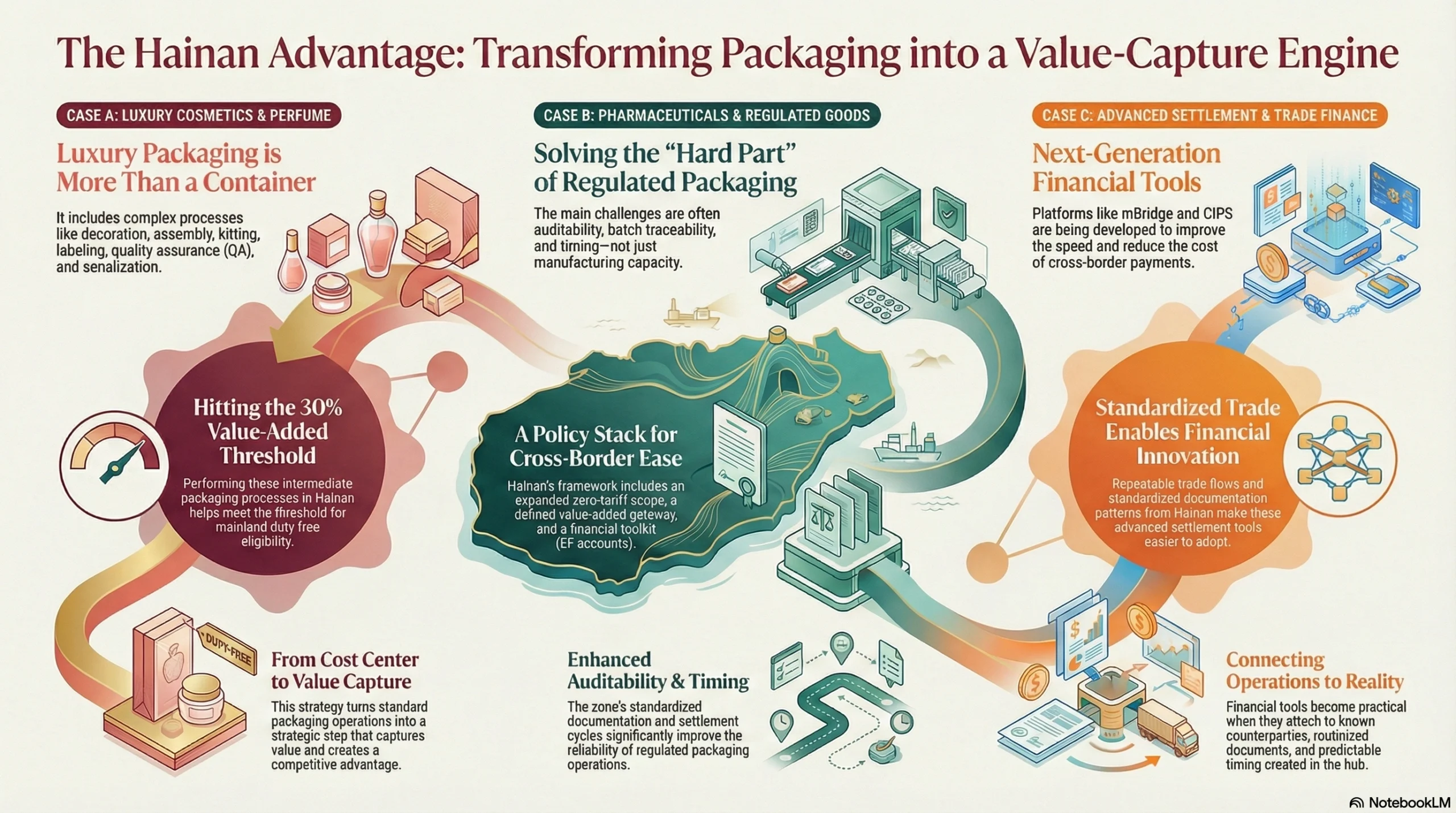

For Jarsking’s marketing audience—procurement, product, and operations leaders in luxury cosmetics, perfume, and pharma packaging—the “Hainan hub” logic becomes most concrete when mapped onto packaging-heavy value chains.

Case A: Luxury cosmetics/perfume packaging supply chains (Jarsking-relevant).

Luxury packaging is not only containers; it includes decoration, assembly, kitting, labeling, QA, serialization, and the documentation layer that brand owners increasingly treat as part of compliance and consumer-trust architecture. These are precisely the kinds of modular intermediate processes that can be performed in a policy zone like Hainan to help meet the 30% value-added threshold for mainland duty-free eligibility—turning “packaging operations” into a value-capture step rather than a pure cost center. Source

Case B: Pharma and regulated goods pathways.

Regulated goods often require validated documentation, batch traceability, and controlled packaging operations. While the Hainan customs announcement does not enumerate pharma workflows line-by-line, the policy and financial stack is clearly oriented toward making cross-border operations easier to execute inside the zone: expanded zero-tariff scope, a defined value-added gateway for mainland entry, and a finance toolkit (EF accounts) to support cross-border flows. This matters for regulated packaging because the “hard part” is often not manufacturing capacity but auditability and timing—areas that improve when zones standardize documents and settlement cycles. Source Source

Case C: Settlement + trade coupling (mBridge/CIPS).

mBridge is described by the BIS as an MVP-stage, governance-backed platform aimed at improving cross-border payment speed and cost, and serving as a testbed for interoperability and new use cases. CIPS, meanwhile, demonstrates scale and operational throughput in PBOC reporting. When a trade hub like Hainan produces repeatable trade flows and standardized documentation patterns, settlement tools become easier to adopt because they attach to operational reality (known counterparties, routinized documents, predictable timing) rather than “innovation curiosity.” Source Source Source

Geopolitical Implications—A China-Centric ASEAN Economy?

The optimistic view is deeper integration and lower friction; the pessimistic view is dependency. A useful way to frame this without overstating outcomes is to treat Hainan as a choice architecture: it makes certain trade workflows—China-linked processing, compliance, and settlement—easier to execute, which can gradually shape corporate behavior even if firms remain multi-hub and multi-currency.

Within the international monetary system, the ECB’s annual review notes that “some countries have been actively exploring alternatives to traditional cross-border payment systems” and that there is evidence of a link between shifts in invoicing patterns and geopolitical alignment in certain cases, even while global aggregates remain broadly stable. This matters because it suggests the “system competition” is likely to appear first as corridor-by-corridor adjustments (how firms invoice, where they clear, which rails they use), rather than a sudden replacement of incumbent infrastructures. Source

Hainan’s role in that environment is not necessarily to “force” alignment, but to make a China-linked trade workflow cheaper and more operationally repeatable through incentives (zero-tariff expansion; 30% rule) and financial tooling (EF accounts and related facilitation). Over time, if the zone standardizes documentation and settlement patterns, it lowers switching costs for firms to route more intermediate value creation through Hainan—exactly the mechanism by which an “industrial chain reconfiguration” can occur without requiring headline-grabbing geopolitical declarations. Source Source

Implications for Global Economic Order

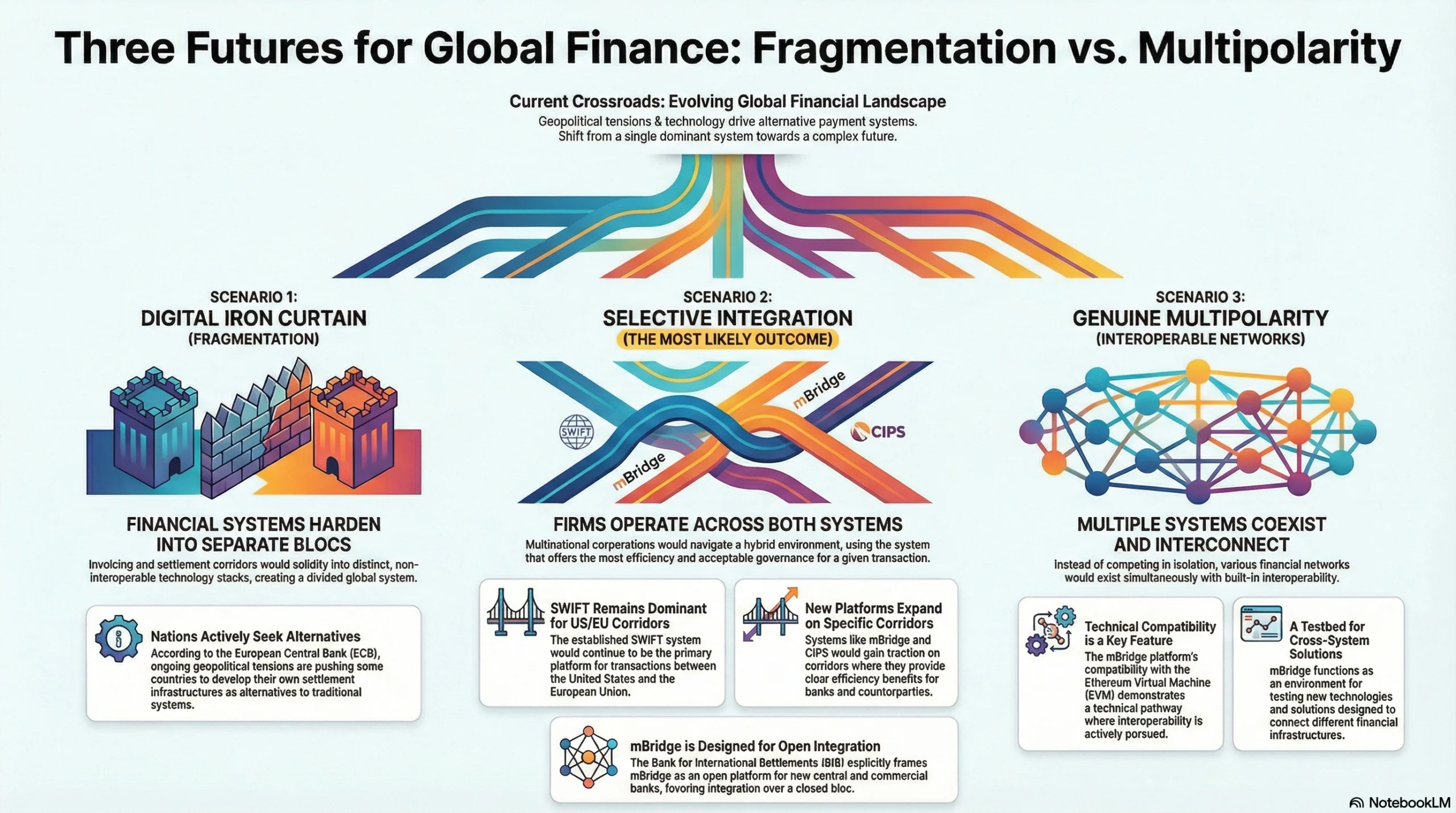

Fragmentation vs. Multipolarity—Three Scenarios

Scenario 1: Digital Iron Curtain (fragmentation).

Invoicing and settlement corridors harden into separate stacks. The ECB notes that some countries have been actively exploring alternatives to traditional cross-border payment systems in an environment of continuing geopolitical tensions, and it discusses the emergence of alternative settlement infrastructure initiatives. Source

Scenario 2: Selective Integration (most likely for multinationals).

Firms operate in both systems. SWIFT remains dominant for US/EU corridors, while mBridge/CIPS expand on specific corridors where counterparties and banks can realize efficiency gains and where governance frameworks are acceptable. The BIS explicitly frames mBridge as open to additional central banks, commercial banks, and private-sector solutions via an MVP legal framework—consistent with selective integration rather than a closed bloc. Source

Scenario 3: Genuine Multipolarity (interoperable networks).

Multiple systems coexist with interoperability. mBridge’s MVP compatibility with the Ethereum Virtual Machine and its role as a testbed for add-on technology solutions and interoperability speaks to a pathway in which interoperability is pursued rather than avoided. Source

What Businesses Should Watch

1) mBridge adoption trajectory.

Track updates on participation expansion, MVP maturation, and real-value transaction readiness signaled by the BIS and HKMA announcements. Source

2) CIPS scaling metrics.

Participants and throughput matter. The CIPS operator’s February 2024 disclosure provides the network footprint (1,497 participants), while the PBOC Payment System Report provides quarterly throughput (2.1292 million transactions; RMB45.19 trillion in Q2 2024). Source

3) Hainan operational execution.

Watch real-world clearance performance and the practical use of the 30% value-added mechanism across industries, as defined in the official “first line/second line” regime. Source

4) EF account scaling and corporate adoption.

The EF account system is a measurable indicator of how much “controlled openness” is being used in practice; PBOC-reported numbers provide a baseline to track. Source

5) RMB share in global payments.

SWIFT RMB Tracker remains one of the most transparent periodic indicators of RMB usage in global payments flows. Source

CONCLUSION: A New Chapter, Not the Final Chapter

Hainan’s customs closure is more than a regional development milestone; it is infrastructure for what Chinese strategists describe as a “second division of labor system”—a parallel set of trade and financial pathways that can operate alongside the incumbent postwar order. But treating this as a simplistic “China vs. West” binary misses the operational reality facing businesses: we are moving toward overlapping systems that coexist, compete, and sometimes interoperate.

Four final insights matter most for corporate strategy:

1) Parallel systems, not replacement.

The Fed’s 2025 analysis makes clear that dollar dominance is still supported by market depth, strong institutions, and safe-asset demand. That suggests the USD system remains foundational. Source

At the same time, SWIFT data show RMB payment share rising gradually—still small, but trending upward. Source

2) Infrastructure is the key lever.

China’s strategy appears focused on building usable rails: mBridge’s MVP architecture aims to reduce cross-border payment friction with a governance framework and rulebook, and CIPS continues scaling participants and throughput. Source

3) Hainan converts geopolitics into supply-chain design.

Hainan’s “first line/second line” model, expanded zero-tariff coverage, and 30% value-added rule create a direct incentive for firms to redesign the location of intermediate processing and packaging steps—especially for China-bound goods. Source

4) The next five years are about trust vs. efficiency.

The ECB shows invoicing patterns remain stable, implying trust and network effects dominate. Source

Meanwhile, mBridge is designed to win on efficiency—instant settlement, lower operational complexity, and an architecture meant to be extended by additional participants and private-sector solutions. Source

For Jarsking’s global B2B audience, the practical takeaway is this: Hainan is a signal that China is building alternative infrastructure without declaring isolation. Companies that treat the future as “one system forever” will be surprised. Companies that design supply chains and treasury workflows to operate across overlapping systems—especially China-linked corridors—will be better positioned to compete. Source

FAQs

Hainan FTP is being positioned as a policy-engineered interface where customs rules and financial facilitation make it easier to route intermediate value-added steps (processing, compliance packaging, documentation) through a China-administered zone before goods enter the mainland market under “second line” controls. The concept matters because it can shift where value is captured along China–ASEAN supply chains by changing incentives and reducing operational friction. Source

The “first line” refers to the interface between Hainan and areas outside China’s customs border, while the “second line” governs movement from Hainan into the mainland. Under the island-wide special customs operations, zero-tariff coverage expands from 21% to 74% of products, and goods processed in Hainan can be sold to the mainland duty-free if value-added reaches 30%—creating clear incentives to perform packaging, assembly, QA, and compliance steps in Hainan. Source

EF accounts are presented as a financial tool supporting Hainan’s cross-border trade and investment convenience under the FTP regime. Their relevance is operational: they help firms manage cross-border funds movement in a controlled policy environment. By end-October 2025, 11 banks in Hainan had opened 658 EF accounts, handling 268.9 billion yuan in transactions across 80 countries/regions—signals of real adoption rather than a purely conceptual policy. Source

CIPS functions as cross-border RMB settlement infrastructure, and its relevance is measurable throughput. The PBOC’s Payment System Report (Q2 2024) reports that CIPS processed 2.1292 million transactions totaling RMB45.19 trillion, demonstrating scale that can support real trade settlement flows—especially if Hainan’s documentation and customs routines make corridor trade more standardized and repeatable. Source

Project mBridge is a multi-central bank digital currency (CBDC) platform initiative designed to explore faster, cheaper cross-border settlement using distributed ledger technology, with an explicit governance/legal framework and MVP-stage readiness. It is best understood as a complementary settlement architecture experiment (especially for wholesale/corridor use cases), while CIPS is an operational RMB payment/settlement system and SWIFT is a global messaging and financial community network used for many transaction types. Source Source Source

The blog’s core argument is coexistence and optionality rather than instant replacement. The ECB notes ongoing geopolitical tensions, continued exploration of alternatives to traditional cross-border payment systems, and evidence of links between invoicing pattern shifts and geopolitical alignment in certain cases—while overall global aggregates remain broadly stable. This supports a “parallel rails” interpretation: firms may add RMB/CIPS and CBDC experiments as options for specific corridors, not abandon incumbent systems wholesale. Source

For Jarsking’s marketing audience—procurement, product, and operations leaders in luxury cosmetics, perfume, and pharma packaging—the “Hainan hub” logic becomes most concrete when you map it onto packaging-heavy, documentation-heavy workflows. The policy mechanics create incentives to move modular intermediate steps (e.g., decoration, kitting, labeling, QA/inspection, serialization readiness, compliance documentation packaging) into Hainan so that finished or semi-finished goods can qualify for duty-free entry to the mainland once the 30% value-added threshold is met.

In parallel, the PBOC’s EF account system is positioned as a facilitation layer for cross-border flows—helpful for packaging programs that often involve multi-country sourcing, iterative sampling cycles, and frequent small-to-mid settlement events. In this framing, Hainan’s “hub” value is less about ports and more about bundling customs + compliance + payments into a repeatable operating model that procurement and ops teams can standardize across SKUs and suppliers. Source Source